Over the past several years there has been increased public discussion of manufacturing, particularly of ‘reshoring’ in the manufacturing sector. The consensus is that a sector-wide move in that direction is necessary, to reverse the effects of previous decades when much of the US manufacturing plant was moved abroad, to Mexico or East Asia.

Pick the best stocks and maximize your portfolio:

While reshoring remains more of a policy conversation than a full-scale movement, it has nonetheless influenced recent federal elections. It’s no coincidence that newly re-elected President Trump is a strong advocate of pro-business measures, such as deregulation, corporate tax cuts, and protective tariffs — all of which could support reshoring efforts.

The prospect of the second Trump term, along with the downward trend in interest rates and several pro-business legislative initiatives previously signed by the outgoing Biden administration, has prompted Jefferies analyst Saree Boroditsky to adopt a bullish stance on the manufacturing sector.

“We see a recovery in manufacturing sentiment bolstered by the potential for lower interest rates, reduced corporate taxes, and deregulation. This should drive higher capex, with spending typically following sentiment by 1-2 quarters. Pro-business policies should build on the megatrends already in place from government (CHIPs, IRA, IIJA) investment… We are focusing our 2025 picks largely on stocks with leverage to factory investment and automation,” Boroditsky stated.

Translating this optimism into action, Boroditsky has identified two specific stock picks that are poised to benefit from these trends. We ran them through the TipRanks database to see what sets them apart.

Regal Rexnord ( RRX )

The first stock we’ll look at is a specialized manufacturing company, Regal Rexnord. This firm produces technology and tools that “power, transmit, and control motion.” Specifically, Regal Rexnord is primarily a maker of a wide range of electric motors, industrial powertrains, and air-moving subsystems. The company’s product portfolio also contains power transmission components, automation controls and actuators, and precision motors.

This lineup of motors and power transmission products has applications in an even wider array of end markets. Regal Rexnord finds its customers in niches from factory automation to warehousing, with the aerospace, alternative energy, construction, data center, medical, mining, and general industrial sectors in between—to give just a part of the company’s reach. The firm, which is based out of Milwaukee, Wisconsin, is organized into three divisions: industrial powertrain solutions, power efficiency solutions, and automation & motion control.

Regal Rexnord maintains its global reach with a network of facilities worldwide. The company has manufacturing, sales, and service offices and centers across the globe, employing approximately 30,000 people. Altogether, their efforts generated $6.2 billion in sales in 2023—although the top line has been trending down in recent quarters.

The last reported quarter was 3Q24. Regal Rexnord reported a total of $1.477 billion in revenues for the quarter, down 11% from 3Q23 and some $50 million below expectations. At the bottom line, the company’s non-GAAP EPS figure of $2.49 was a penny better than had been anticipated. We should note here that even though the company’s revenues have been slipping in recent quarters, earnings showed quarter-over-quarter gains in both Q2 and Q3 this year.

Boroditsky, in her write-up on RRX for Jefferies, sees room for more earnings growth, and goes to some length to explain why: “RRX is a leader in motor and power transmission systems with a margin story still playing out and a portfolio better positioned to capture growth once the industrial backdrop improves. EBITDA margins are expected to exit 2025 at ~25% (~300bps of improvement vs. 2024E) as RRX realizes $65m in acquisition synergies in 2025, mostly related to further rationalizing the global footprint. M&A activity has resulted in a portfolio with ~50% exposure to secularly growing verticals which, combined with organic initiatives, is expected to drive more substantial growth than the business saw historically. Given both margin and top-line levers, we think RRX will be able to compound EPS at a double-digit rate over the next few years.”

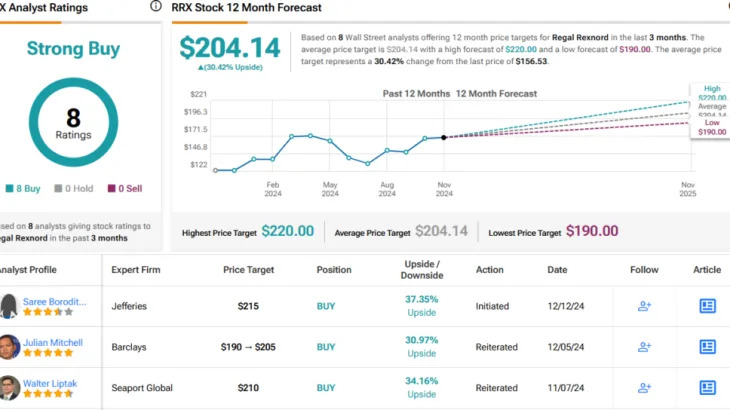

The analyst quantifies her stance with a Buy rating and a $215 price target that suggests a one-year upside potential of 37%. (To watch Boroditsky’s track record, click here )

Regal Rexnord has earned a unanimous Strong Buy consensus rating from the Street’s analysts, based on 8 recent positive reviews. The shares are priced at $156.53 and their average price target, $204.14, implies a share appreciation of 30.5% in the year ahead. (See RRX stock forecast )

ESAB Corporation ( ESAB )

Now based in Maryland, ESAB Corporation, the second stock on our list, was founded in Sweden in 1904. The company is known as a manufacturer of fabrication technologies and industrial gas control systems. While neither of these specialties is a ‘household name,’ both are vital in the industrial world, making possible the machine tools, high-pressure gasses, cutting torches, and welding tools that so many other industrial niches depend on.

ESAB’s fabrication side offers customers more than 40 well-known brands and is based on 28 manufacturing facilities around the world. The company’s gas control systems, acquired through the purchase of GCE in 2018, have approximately 6,000 distributors globally. All told, ESAB employs over 9,000 people across 150 countries and boasts a market cap of $7.7 billion.

Turning to the financial results from ESAB’s last quarterly report, we find that the company tallied $673 million in sales for 3Q24. This was down by 1.2% from the prior-year period but was more than $52 million better than the estimates. On earnings, ESAB realized $1.25 in non-GAAP EPS, beating expectations by $0.13. The company saw its adjusted EBITDA margin expand y/y by 130 basis points in the quarter, to reach 19.6%. ESAB has set a 2028 strategic target of 22% for that margin.

Setting out the Jefferies view here, Boroditsky writes of this company, “ESAB is a leading provider of welding solutions that should compound earnings at a midteens rate including capital deployment. Top-line organic growth is driven by refreshed and expanded equipment offerings and secular tailwinds in automation. The company sees significant opportunities for industry-consolidating M&A, particularly in the gas equipment space which is forecast to grow at a mid-single-digit rate organically. We expect strong margin improvement from cost initiatives and revenue growth (improved operating leverage and margin-accretive mix shift). The combination of top-line and margin improvement should drive a low teens EPS CAGR over the next three years.”

Boroditsky’s stance on ESAB supports her Buy rating on the stock, while her $160 price target implies the shares will gain 29% over the next year.

Overall, this manufacturing company gets a Moderate Buy consensus rating, based on 5 Buys, 2 Holds, and 1 Sell set in recent months. The shares have a trading price of $123.88 and an average price target of $135.38, indicating room for a gain of 9% in the months ahead. (See ESAB stock forecast )

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy , a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.