(Bloomberg) -- Bond traders are taking chips off the table, opting for a more neutral stance before Wednesday’s US consumer-price data, which will be decisive in setting expectations for whether the Federal Reserve cuts interest rates again this month.

JPMorgan Chase & Co.’s weekly survey on Tuesday showed the bank’s clients have shifted to a neutral stance on Treasuries from the strongest long bias this year, stepping back following a three-week rally in US government debt.

The November consumer-inflation reading due Wednesday is expected to show a small acceleration on both a monthly and annual basis. The report is in focus after Fed Governor Christopher Waller earlier this month said that data due before officials meet Dec. 17-18 could make the case for holding rates steady, although he’s inclined to reduce rates again for the third consecutive time.

While swaps markets are pricing in a roughly 80% chance of a quarter-point Fed cut this month, the resilient US economy — and speculation that the policies of President-elect Donald Trump will spur quicker inflation — have opened the door to bets on a pause at some point. Beyond Dec. 18, markets are reflecting roughly two additional quarter-point reductions by the end of next year.

The market for fed funds futures, which closely tracks expectations for the Fed, showed a similar move to trim wagers on a rate cut this month. The latest open interest data dropped in both the January and February futures, in a sign that investors are unwinding long positions.

Here’s a rundown of the latest positioning indicators across the rates market:

JPMorgan Treasury Client Survey

In the week to Dec. 9, JPMorgan clients shifted positioning into neutral and out of longs, while the level of short positions was steady. Over the period, bullish positioning dropped 6 percentage points and neutrals increased the same amount. Outright long positions dropped back to the same level seen a couple of weeks ago, while neutrals are the most elevated in two weeks.

Treasury Options Premium Close to Neutral

The cost to hedge bond-market moves using options remained balanced over the past week, with most tenors trending around neutral. That means the expense of protecting against a rally is equal to that of hedging for a selloff. In a shift from a recent surge in bearish hedges, stand-out flows in Treasury options over the past week targeted lower yields. Flows included a $7 million premium wager looking for a 3.9% 10-year by the end of January — from roughly 4.2% now — and a structure targeting 4.05% on the 10-year by the end of this week.

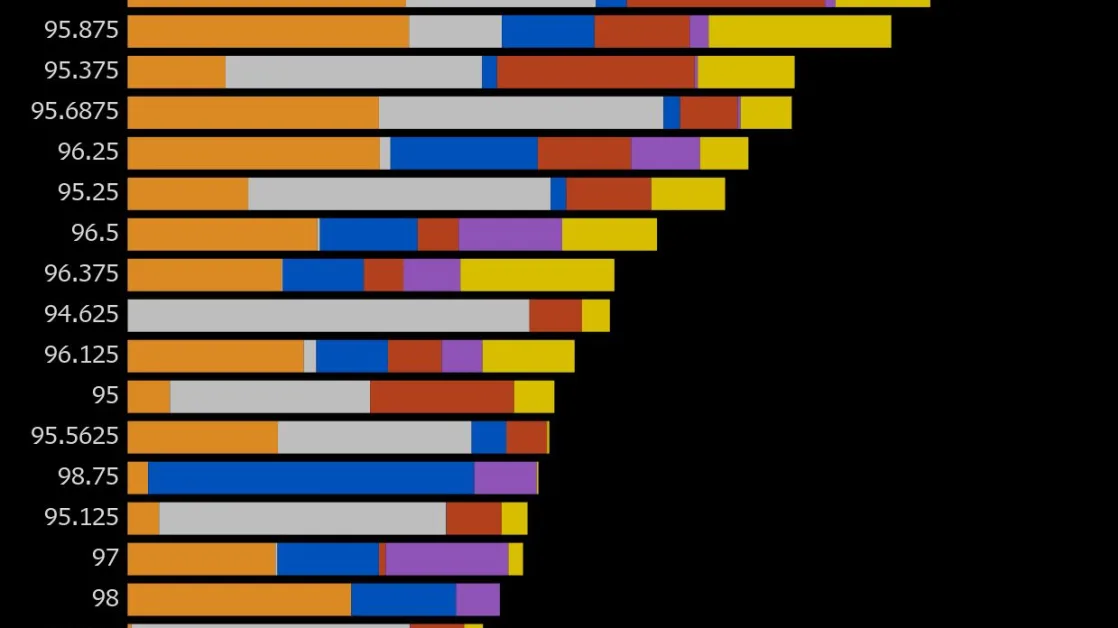

Most Active SOFR Options

Over the past week there has been a mix of both new positioning and liquidations across a range of SOFR options. For new positioning, open interest has jumped most in the 95.9375 and 96.125 strikes following recent flows, including a large buyer of the SFRH5 95.5625/95.9375/96.125 1x3x2 call fly, a dovish hedge targeting a couple of quarter-point rate cuts by the end of the first quarter. Heavy liquidation was seen over the past week in the 95.625 strike following flows including a large seller of the SFRZ4 95.5625/95.625/95.6875 call fly.

SOFR Options Heatmap

In SOFR options out to the June 2025 contract, the 95.50 strike is still the most populated. Recent flows around the strike have included a SFRZ4 95.50/95.625 call spread buyer and the SFRZ4 95.5625/95.50/95.4375/95.375 put condor. New downside seen over the past week has been in the SFRZ4 95.50/95.5625 2x1 put spread, adding to the open interest in the strike.

CFTC Futures Positioning

Asset managers added to net-long duration positioning across Treasury futures over the week to Dec. 3 while hedge funds covered a net duration short. Asset managers added around 53,000 10-year note equivalent futures of a net duration long while hedge funds covered approximately 22,000 10-year note equivalents of net shorts. In SOFR futures, both investor types covered net long positions, flipping net short for the first time since July.