There’s been something of a sea change in the economic outlook for 2025, in the aftermath of last month’s election. The prospect of a second Trump administration, with his known preference for deregulation and tax cuts, has market watchers expecting a growth-friendly environment.

Pick the best stocks and maximize your portfolio:

Desh Peramunetilleke, Jefferies’ Global Head of Quantitative Strategy, notes that reduced regulation, combined with the potential for lower corporate tax rates, could significantly boost the biotech sector, with smaller biotech stocks poised to benefit the most.

“Our recent analysis concluded with a near-term preference for smaller-cap biotech names in the US… Trump’s win brings new market dynamics into play. Firstly, his policies concerning taxation and government regulation imply a more risk-on environment, encouraging investments and M&A activity. This is conducive for rerating of the smaller biotech names,” Peramunetilleke explained.

Following his lead, Jefferies stock analysts have picked two small biotech stocks with strong upside – including one with a potential gain of nearly 1,000%.

In fact, Jefferies analysts are not the only ones singing the praises of these stocks. According to the TipRanks database , they are both rated as ‘Strong Buys’ by the analyst consensus. Let’s dive into what makes these stocks such compelling investment opportunities right now.

Metagenomi (MGX)

The first Jefferies pick we’re looking at is Metagenomi, a biotech innovator unlocking the potential of gene editing through the power of metagenomics. This approach focuses on identifying microbial genetic systems shaped by nature and adapting their enzymes into precise tools for addressing various diseases. By leveraging the vast genetic diversity found in nature, Metagenomi aims to develop therapeutic solutions that could contribute to meaningful advancements in modern medicine.

The company’s flagship candidate, MGX-001, is a novel therapeutic agent targeting hemophilia A (hemA). Last quarter, Metagenomi announced an important achievement, reaching durable Factor VIII activity levels over a one-year period in an NHP (non-human primate) study. The company has gone on to initiate IND-enabling activities for MGX-001 as a regulatory step toward moving the program to the human clinical trial stage.

But Metagenomi isn’t stopping there. Through a partnership with Ionis Pharmaceuticals, the company is integrating RNA-targeted therapeutics with its gene-editing systems. This collaboration focuses on cardiometabolic development programs, initially targeting four conditions, including transthyretin amyloidosis (TTR) and refractory hypertension (AGT). Currently in the lead optimization phase, these programs have demonstrated proof-of-concept in rodent models. Looking ahead, Metagenomi plans to nominate one to two development candidates by 2025.

With early clinical progress and a share price of just $1.85, Jefferies analyst Maury Raycroft believes MGX shares represent a high-potential opportunity.

“We continue to view MGX stock as undervalued given: 1) derisking 1-yr NHP data, which sets the stage for durable FVIII expression for hemA; 2) broad platform play with multiple genome editing capabilities along with in-house GMP manuf capabilities — could facilitate multiple BD deals with initial PoC studies; 3) IONS-partnered cardiometabolic programs advancing toward DC nomination in 2025 with rodent POC achieved,” Raycroft noted.

“Though first human testing may not begin until 2026 in lead hemA and PH1 programs, animal PoC data in >2024 across their portfolio along with potential BD deals could further strengthen the platform, potentially driving the shares higher given broad applicability and valuation at a discount,” the analyst added.

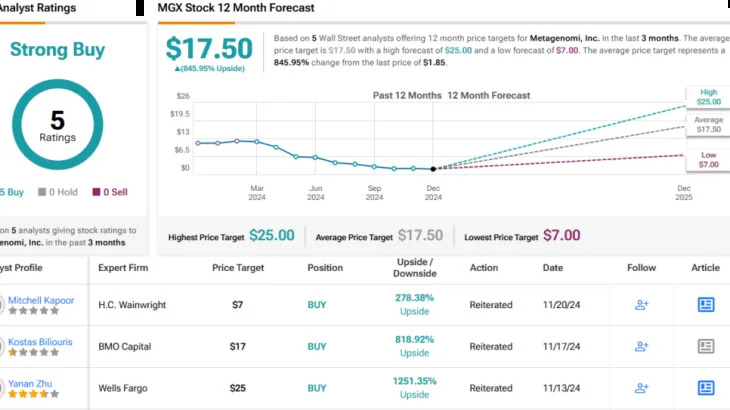

So, how high could this go? Raycroft gives MGX a Buy rating, with a price target of $21, suggesting a remarkable 1,035% upside potential. (To watch Raycroft’s track record, click here )

Like Raycroft, other Wall Street analysts are optimistic about this biotech’s prospects. With 5 Buys assigned in the last three months, the message is clear: MGX is a Strong Buy. Should the $17.50 average price target be met, a twelve-month gain of ~846% could be in the cards. (See MGX stock forecast )

Structure Therapeutics (GPCR)

Next on Jefferies’ radar is Structure Therapeutics, a clinical-stage biopharmaceutical company dedicated to developing new treatments for chronic conditions, particularly metabolic and pulmonary diseases that have, in the jargon, ‘high unmet medical needs.’

Structure’s technology is based on G-protein coupled receptors (GPCRs), which make up the largest family of human membrane proteins. GPCRs are involved in most aspects of human physiology, and more than 100 of these proteins are acted on by some 475 drugs on the market. While that sounds like a lot, there is still a large addressable market here – more than 220 of these proteins remain available as targets for clinical research.

The company’s leading drug candidate is GSBR-1290, an orally-dosed small molecule agonist of the glucagon-like-peptide-1 (GLP-1) receptor. GLP-1 has been validated as a useful drug target in the treatment of both obesity as a metabolic condition and type 2 diabetes mellitus. The drug was developed on Structure’s platform as a biased GPCR agonist, selectively activating the G-protein signal pathway. GSBR-1290 is currently under investigation in clinical trials as a treatment for obesity.

These trials have advanced to the Phase 2 stage, and in June, the company released a set of positive data from the earlier Phase 2a study. Last month, Structure announced that the follow-up trial, the Phase 2b ACCESS study, had begun dosing patients.

Beyond GSBR-1290, Structure is progressing with the development of an orally administered small molecule amylin receptor agonist for obesity treatment. The company aims to finalize a development candidate by year-end.

Covering this company for Jefferies, analyst Roger Song notes the success – and the future potential – of GSBR-1290, writing of the program: “OW data reaffirms class leading efficacy of GSBR1290, with PK/PD modeling suggest long-term WL in line with orfo/ sema supporting ‘1290 into Ph2b in 4Q24… With promising Ph2a 12W data on hand, and Ph2b 36W data expected in 4Q25, we see ‘1290 is leading new-gen small molecule incretin space, and can potentially set the new bars if we can see directionally higher WL with higher doses and improved GI tolerability with 120mg dose.”

Song has also taken note of the amylin program and is optimistic about the company’s ability to develop a competitive drug candidate: “Amylin program excitement continues, with first DC to announce YE24 and multiple others in planning. Comp data from AZD5004 and AZD6234 both underwhelming, further solidifying GPCR leading position with robust pipeline.”

The potential inherent in these two programs led Song to rate Structure shares as a Buy, while his $79 price target points toward a one-year upside potential of ~137%. (To watch Song’s track record, click here )

All in all, Structure has picked up 9 unanimously positive analyst reviews, supporting a Strong Buy consensus rating. The stock is currently trading for $33.35, and its $88.56 average price target implies a gain of 165% in the next 12 months. (See GPCR stock forecast )

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy , a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.