Heading into 2025, market watchers are starting to plan strategies based on a return to pro-business and deregulatory policies. The prospect of lower inflation and lower interest rates promises relief from debt pressures, which will be beneficial for lenders and other financial service firms.

Don't Miss our Black Friday Offers:

This will bring investors’ sights to bear on BDCs, business development companies. These are investment firms, operating outside the traditional banking system but making capital and credit available to small- and mid-sized businesses. It’s a vital niche, that supports a main driver of the US economy.

One key feature of BDCs, that makes them attractive to their investors, is their propensity to pay out high dividends. These companies offer capital, which means they need to bring in capital – and their investors expect a return. Dividends make a convenient mode for BDCs to return capital to their own investors. It’s a feature that makes these companies a solid addition to any set of portfolio dividend stocks.

Wells Fargo analyst Finian O’Shea is paying close attention to this sector. In a recent report, O’Shea highlighted the potential in BDCs, stating, “BDCs appear to offer an improved relative entry point today in the world of balance sheet financials. A developing scenario of higher for longer with a strong economy for example could re-emerge for an attractive set up. This assumes credit losses are benign which has been true overall but with growing dispersion.”

Getting into specifics, the Wells Fargo analyst makes it clear that he likes two BDC dividend stocks in particular – including one that yields as high as 15%, a powerful return by any standard. We’ve used the TipRanks platform to look up the details on these two BDCs. Let’s take a closer look.

Runway Growth Finance Corporation ( RWAY )

The first stock on our list is Runway Growth Finance Corporation, a BDC focused on minimally dilutive venture capital. Runway’s activities in particular are directed towards venture debt, providing capital support for new companies in the technology, healthcare, and consumer niches. The company’s strategy, by avoiding dilution of the client firms’ stock, allows those firms’ founders and early investors to maintain their ownership, a key point for many startups.

Runway Growth has been supporting startup firms since 2015, and in that time it has backed more than 60 companies, with 91 deals totaling some $3 billion in loan commitments. The target companies typically fit a profile; they are backed by venture capital or private equity, typically show $10 million to $20 million in annual revenue with high year-over-year growth, and are seeking loans in the range of $10 million to $75 million. Runway describes its mission as supporting passionate entrepreneurs as they build innovative businesses.

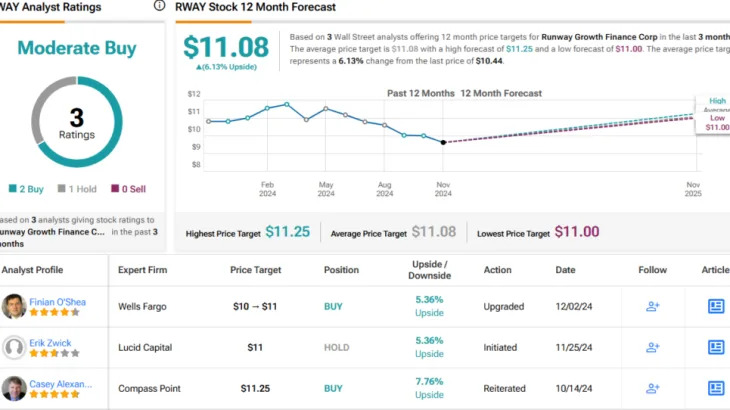

On the dividend, Runway last declared its common share payment on November 5 for 40 cents per share. The dividend was paid out on December 2. Its annualized rate of $1.60 per share gives a forward yield of more than 15.3%.

The company’s dividend was supported by its recent financial results. In 3Q24, Runway saw a total investment income of $36.7 million, although that figure missed expectations by $1.32 million. At the bottom line, Runway’s net investment income came to $15.9 million, which translated to 41 cents per share. While that missed the forecast by 4 cents per share, it was enough to fully cover the regular dividend payment.

In his coverage of this company for Wells Fargo, analyst O’Shea notes that this BDC is near the bottom of a cycle – and that the firm’s current condition offers a sound opportunity to buy in. He writes, “RWAY shares have lagged the industry by ~18% on a total return basis YTD and trade at 0.78x book, and could re-rate upon a shift from what is likely ‘peak pessimism and uncertainty’ with what we see as a more right-sized consensus NOI estimate… We’re upgrading RWAY (to OW from EW) as we believe sentiment has likely reached the bottom, and its valuation presents more potential upside than downside risk.”

Along with his upgraded Overweight (Buy) rating, O’Shea puts an $11 price target on the stock that implies a 5% gain in the coming months. Add in the dividend yield, and the total one-year return on these shares can climb above 20%. (To watch O’Shea’s track record, click here )

There are only 3 recent analyst reviews on file for RWAY stock, and they include 2 Buys to 1 Hold for a Moderate Buy consensus rating. The shares have a current trading price of $10.44 and their $11.08 average price target points toward a one-year gain of 6%. (See RWAY stock forecast )

Ares Capital Corporation ( ARCC )

The next stock on our BDC list is Ares Capital Corporation, an important credit provider in the US small business sector. This is an important niche in financial services, as small- and mid-sized businesses are the traditional engine of the US economy. Ares Capital Corporation has 20 years’ experience in the field, and provides an essential service for its client firms – it provides the resources that they need to survive.

Ares Capital Corporation has, in its two decades of operations, put together a substantial portfolio, with a fair value estimated at $25.9 billion. This portfolio is composed of 535 companies, which in turn are backed by 240 private equity sponsors. Dipping into the drill-downs, we find that nearly 53% of the portfolio is comprised of first lien senior secured loans. Second lien senior secured loans and preferred equity securities each make up approximately 10.5% of the total. By industry composition, Ares Capital’s portfolio is just over one-fourth software and services companies; health care services firms make up 12.8%, and commercial and professional services companies make up 10.7% of the total.

The return on this portfolio makes up Ares’ income stream, which in the last reported quarter, 3Q24, came to a quarterly total investment income of $775 million. This figure was up more than 18% year-over-year, and was almost $1.7 million better than had been anticipated. The company’s bottom line, a non-GAAP EPS of 59 cents, was 1 cent lower than the forecast.

Despite missing on EPS, the company’s income still easily covers the dividend. Ares Capital Corp. declared a 48-cent common share payment on October 30, for a December 30 payout. The annualized rate of $1.92 per common share gives a substantial forward yield of ~8.7%.

O’Shea, in looking at this stock, is impressed by Ares Capital’s sound performance and the high quality of its portfolio. He says of the company, “In a market where many more average performers are at or near book value, ARCC gets the award for reliability, which it has demonstrated yet again through best-in-class credit performance throughout the Fed’s campaign. Credit performance YTD 2024 and since 2022 are both #1 in our coverage, where gains from equity investments, including Heelstone, have helped cover credit losses…”

Describing the opportunity here, the analyst adds, “Thematically, we see a lower base rate environment as a likely positive for ARCC, which has an impressive record in junior / structured credit. Lower rates may lead to an expansion of this opportunity set for ARCC.”

This is another stock that gets an upgrade from the Wells Fargo analyst; his Overweight (Buy) rating here is a bump up from Equal Weight. O’Shea’s price target, of $23, suggests that the stock will gain 4% by this time next year. With the dividend yield, the total return on ARCC, for the coming year, may reach as high as almost 13%.

The Street in general likes this stock, as shown by the Strong Buy consensus rating – a rating that is supported by 10 reviews with a breakdown of 8 Buys to 2 Holds. The shares are priced at $22.10, and the $22.40 average target price implies they will stay rangebound for the time being. (See ARCC stock forecast )

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy , a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.