Love them or loathe them, the ultrawealthy share one undeniable trait: they are remarkably disciplined with their money. The novelist Herman Wouk put it best, in his book Don’t Stop the Carnival, saying of the wealthy Lester Atlas, “He acted on a clear hard rule: never part unnecessarily with a dollar.”

Don't Miss our Black Friday Offers:

Today’s high-net-worth individuals live by that principle, often relying on family offices –specialized private money management firms – to safeguard and grow their wealth. These family offices strategically invest in a range of assets, including public equities, hedge funds, and increasingly, private equity.

This growing interest in private equity has been highlighted in a recent study by investment bank Bastiat Partners and private equity firm Kharis Capital. The study reveals that nearly 40% of family offices see private equity as a “core component” of their investment strategies over the next two years. Similarly, a September survey from Campden Wealth and RBC Wealth Management found family offices favor private equity and venture capital for their long-term risk-adjusted returns. In fact, 42% anticipate increasing their private equity exposure this year, compared to 19% planning to expand their investments in public stocks.

As private equity gains traction among family office investors, Wall Street analysts are paying close attention. According to the TipRanks database , two private equity stocks have emerged as Strong Buy candidates. Let’s take a look into what makes these names stand out in the eyes of top analysts.

Compass Diversified Holdings ( CODI )

We’ll start with Compass Diversified Holdings, a private equity firm that uses its capital to invest in “people, processes, culture, and growth opportunities that drive transformational change.” The company was founded in 1998 and went public in 2006. Today, it boasts a market cap of nearly $1.8 billion and has active holdings in 10 companies.

By the numbers, Compass Diversified is impressive. The company has conducted $9.3 billion in aggregate transactions and realized $1.5 billion in gains since its IPO. The firm manages $3.3 billion in assets and generated nearly $2.06 billion in revenue last year.

More recently, the company reported $582.6 million in 3Q24 revenues, up almost 12% year-over-year and nearly $11 million better than was forecast. The company’s bottom line for the quarter, reported as GAAP EPS, was 8 cents per share—a solid turnaround from the 45-cent loss reported for 3Q23.

Compass Diversified pays out a dividend to shareholders at a quarterly rate of 25 cents per common share. The annualized payment of $1 per share gives a forward yield of 4.2%. The dividend was last paid out on October 24. In addition to its dividend, Compass Diversified supports the share price through a repurchase policy. The current policy, announced in mid-October of this year, allows the firm to repurchase up to $100 million worth of common stock and is valid through this coming December 31.

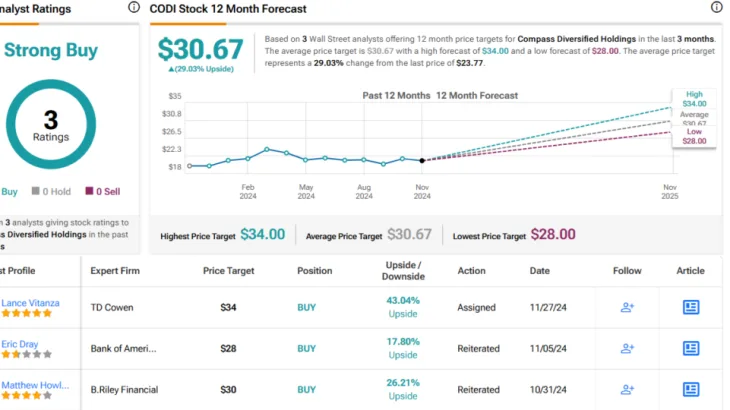

For TD Cowen’s Lance Vitanza, an analyst ranked in the top 2% of Wall Street stock pros, this private equity company presents investors with a solid prospect for continued earnings growth. The 5-star analyst writes, “Compass currently owns and manages an attractive, diversified portfolio of companies consisting of seven branded consumer businesses and three niche industrial businesses. Each portfolio company is believed to be a leader in its respective category or market sector. We see strong earnings growth and multiple expansion as dual drivers. We value Compass primarily via adjusted EPS, which we expect will grow at a three-year CAGR of 20% through FY26.”

Vitanza uses this stance to back up his Buy rating on CODI, while his $34 price target points toward a one-year upside potential of 43%. (To watch Vitanza’s track record, click here )

While this stock only has three recent analyst reviews on record, they are unanimously positive—for a Strong Buy consensus rating. The shares are priced at $23.77, and their $30.67 average target price indicates room for a 29% gain in the next 12 months. (See CODI stock forecast )

Brookfield Business Partners ( BBU )

The second stock we’ll look at is Brookfield Business Partners, a publicly traded subsidiary business of the larger parent company, Brookfield Corporation. The parent firm is a major global investment firm, with more than $1 trillion in total AUM under its asset management branch. Brookfield Business Partners, BBU, acts as the parent firm’s business services and industrial operator, putting capital to work in the Brookfield family.

Brookfield Business Partners has three distinct operational divisions: industrial, infrastructure services, and business services, and these focus on the ownership and operation of a wide range of high-quality product and service providers. The company’s investment portfolio includes 47 names, working in fields such as residential mortgage insurance, technology software, modular buildings, work access, lottery services, advanced energy storage operations, and graphite electrode manufacturing. BBU has been in the business of providing capital and financing in these areas, and more, for nearly a decade, and is based in Toronto, Ontario.

This private equity firm generated just over $55 billion in revenues last year. The company states its primary goal as generating a long-term return for its investors in the range of 15% to 20% from the investments in its portfolio.

In its most recent quarterly report, covering 3Q24, Brookfield Business Partners showed a top line of $9.23 billion and an EPS figure of $1.39. While the revenue total was down nearly 36% year-over-year, the company’s earnings marked a sharp reversal from the prior-year period, when BBU reported a net EPS loss of 20 cents. The company had cash assets at the end of Q3 of just over $3 billion.

This stock has caught the eye of RBC analyst Robert Kwan, who is rated by TipRanks among the top 2% of the Street’s analysts. Kwan explains why BBU is likely to bring continued gains for investors, saying, “Although the units have performed well as of late, we continue to believe that there is significant upside to our estimated net asset value. We think that continued asset monetizations that crystallize asset value as well as allow BBU to reduce holding company debt are likely catalysts that could result in material unit price appreciation.”

The 5-star analyst goes on to put an Outperform (Buy) rating on BBU shares, along with a $32 price target that suggests a 12-month gain of 23%. (To watch Kwan’s track record, click here )

Overall, Brookfield Business Partners has earned a Strong Buy consensus rating, based on 4 unanimously positive recent analyst reviews. The shares are currently trading for $26.05 and have an average price target of $31.50, together implying an upside of 21% on the one-year time horizon. (See BBU stock forecast )

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy , a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.