(Bloomberg) -- The US debt ceiling is once again emerging as the Federal Reserve continues to unwind its balance sheet, putting the central bank in a tough spot — only this time it’s trickier.

The debt limit will be reinstated on Jan. 2, prompting the Treasury Department to deploy a series of extraordinary measures that include spending down its cash pile and reducing the amount of T-bills it issues to preserve its borrowing capacity.

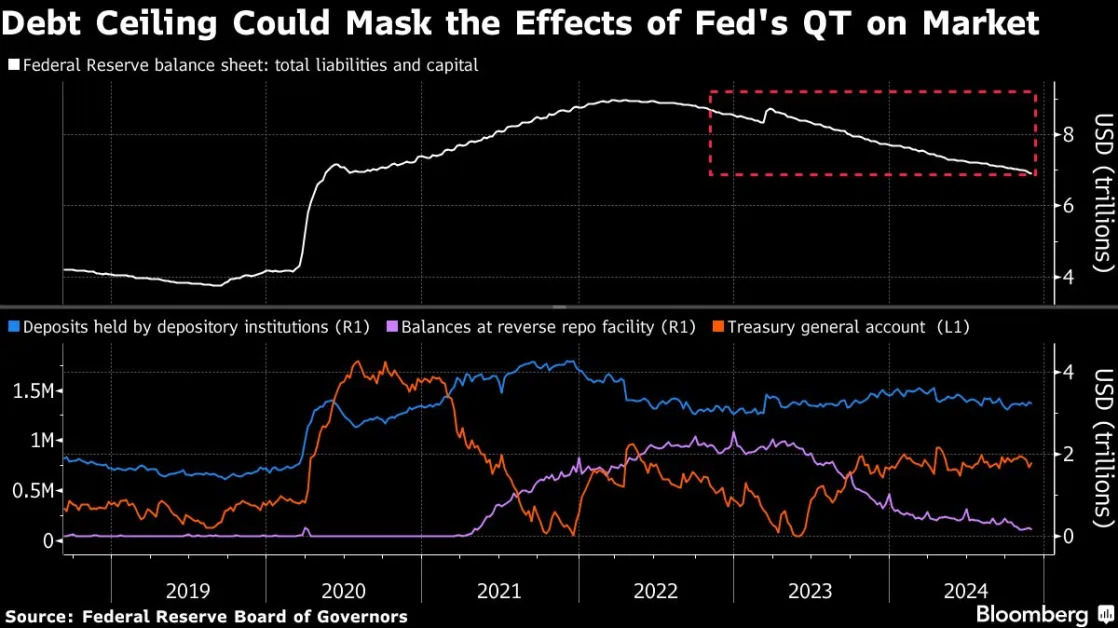

Because the Treasury’s cash balance, known as the Treasury General Account, or TGA, is one of the major liabilities on the Fed’s balance sheet, such measures will boost mainly bank reserves parked at the central bank and demand for the overnight reverse repurchase agreement facility, or RRP. That means markets will be flush with cash as the Fed continues shrinking its own balance sheet in a process known as quantitative tightening, or QT.

Once Congress passes legislation to suspend or lift the debt ceiling, the Treasury will work quickly to rebuild its cash balance, a process that yanks cash out of the financial system. The shifting of money between markets and the government’s checking account risks masking signals that are critical for identifying any strains created by the central bank’s balance-sheet runoff.

“The Fed may be flying blind in monitoring the impact of QT as the debt ceiling starts to pressure TGA balances lower, temporarily increasing reserves in the system,” said Gennadiy Goldberg, head of US interest rate strategy at TD Securities. “This also increases the risk that once the debt ceiling is raised and the TGA sharply increases, reserves are drawn down quickly and lead to outright scarcity.”

Minutes from the central bank’s November gathering showed staff briefed the committee about possible implications of the debt ceiling’s reinstatement.

All this is making it more difficult for market participants and policymakers to determine the end of QT. Two-thirds of respondents to the New York Fed’s Open Market Desk’s Survey of Primary Dealers and Survey of Market Participants expect QT to end in the first or second quarter of 2025, the minutes showed.

During the last debt-limit episode in 2023, the Fed had been running down its balance sheet for less than a year and there was still $2.2 trillion parked in the overnight reverse repo facility — a tool considered a barometer for excess liquidity. Yet, once Congress suspended the ceiling and Treasury rebuilt its cash balance via increased bill issuance, money-market funds fled the RRP. This time around, going into 2025 there’s less than $150 billion there.

That means any rebuild of the TGA will result in a drop in bank reserves. Although the account is currently at $3.23 trillion, a level policymakers consider abundant, market observers are closely tracking the level to assess at what point it will become scarce.

In addition, there’s a greater risk of more volatility because the backdrop of the funding markets is different than last time, according to Morgan Stanley. Since 2023 there’s been a “significant increase” in hedge funds’ long Treasuries positions, with even more collateral sitting outside the Fed and banking system, strategist Martin Tobias wrote in a year-ahead note.

Given that it’s likely the Treasury will have to reduce its bill issuance until the debt cap is raised or suspended, money-market funds will be motivated to park more cash at the RRP despite higher private repo market rates. There were similar frictions in July when dealer balance-sheet constraints and sponsored repo limitations kept usage of the reverse repo facility sticky.

“Capacity constraints, as well as counterparty risk limits have potential to push money market fund cash into the RRP,” impeding the liquidity redistribution process,” Tobias wrote. “This in effect reduces the supply of repo financing at a time when demand” is continuing to increase.

Even as most Wall Street strategists have coalesced around when the Fed balance-sheet unwind should end, it’s been harder to determine when the US government will run out of funds, or the so-called X-date.

Before Donald Trump’s election victory, strategists’ early read placed the X-date at around August 2025. Now, some say it’s more likely that the date will be earlier, sometime in the second quarter, now that Republicans gained control of the White House and Congress.

Still, all of this uncertainty will make the Fed’s ability to gauge the risks of QT on short-term rates all the more challenging. RBC Capital Markets strategists see the central bank halting QT in the second half of 2025, noting that remarks from policymakers suggests the runoff has a ways to go.

Deutsche Bank strategists led by Steven Zeng and Matthew Raskin said policymakers could consider enhanced market monitoring and ensure liquidity backstop tools are ready, further slowing the pace of the runoff, pause QT until the debt-ceiling is resolved or prematurely end the unwind, though they think the latter two options are unlikely.

“Growing the balance sheet is easy,” said Wells Fargo strategist Angelo Manolatos. “Shrinking it is hard.”