(Bloomberg) — A bearish tone is taking hold in the market for interest-rate options, suggesting that bond traders are bracing for Treasury yields to surge anew in the coming weeks.

There has been steady demand for bearish hedges using Treasury-option put structures in January contracts on 10-year notes, which expire Dec. 27. Positioning has also been building over the past couple of days in the February options, which expire Jan. 24, the week of President-elect Donald Trump’s inauguration.

Open interest, or the amount of outstanding positions held by traders, has been building specifically between the 107.50 and 109.50 put strikes in the January and February options. Those levels target a 10-year yield range of approximately 4.45% to 4.75%, relative to roughly 4.3% now. The upper bound of that span would push the yield above its 2024 high of about 4.74%, touched in April.

On Tuesday, an even more bearish position traded, targeting a yield as high as 4.9%, for a premium of $2.5 million. The benchmark yield hasn’t been that high in more than a year.

The wagers are a reminder that even though yields have surrendered the brunt of their post-election advance, investors are well aware of the potential for the so-called Trump trade to gain traction again. The premise of that trade for months has been that his policies including steeper tariffs would quicken inflation and push yields higher. Treasuries fell modestly on Tuesday, bumping up 10-year yields slightly, after Trump threatened to place additional tariffs on US trade partners.

Along with Trump’s first few day’s in office next month, a couple of other events ahead will be key for these options bets. First off, next week’s report on November job figures is projected to show a big jump in employment from the prior month.

Then there’s the Dec. 18 Federal Reserve policy announcement. Traders see it as a coin toss as far as whether officials will cut interest rates by another quarter-point or stand pat amid signs of economic resilience.

Meanwhile, in the cash market, bearish positioning has been growing, according to a survey of JPMorgan Chase & Co. clients, who are now the most short in a month.

Here’s a rundown of the latest positioning indicators across the rates market:

JPMorgan Treasury Client Survey

In the week to Nov. 25, JPMorgan client short positions extended 2 percentage points to the highest since Oct. 28. Neutrals dropped on the week to the smallest since Oct. 21 with long positions also rising by 2 percentage points.

Treasury Options Premium Drifts Toward Puts

The premium to hedge moves in the bond market has drifted closer to favoring puts over recent sessions amid demand for options targeting higher yields over the coming weeks. There has been an influx of buying in options around the January and February 10-year tenors targeting the maturity’s yield rising as high as 4.9%. Tuesday’s action included buying of both January and February puts for a combined premium of $5 million over two trades.

Most Active SOFR Options

Over the past week there has been heavy demand for upside price protection via a wide range of call structures around December SOFR options. Standout flows for new risk have included large buyers of the SOFR Dec24 95.5625/95.625/95.6875 call fly and SOFR Dec24 95.625/95.6875 call spread as positioning builds to target a rate cut at the December Fed policy meeting.

SOFR Options Heatmap

In SOFR options out to the June 2025 tenor, the 95.50 strike is still the most populated. Recent flows around the strike have included a SFRZ4 95.50/95.625 call spread buyer and the SFRZ4 95.5625/95.50/95.4375/95.375 put condor. On Monday the SFRZ4 95.50/0QZ4 96.3125 call spread was bought as a bull steepener structure. The 96.00 strike is also well-populated where a large amount of Dec25 calls remain. Recent flows around the strike have included SFRH5 96.00/96.25/96.375 broken call flies bought.

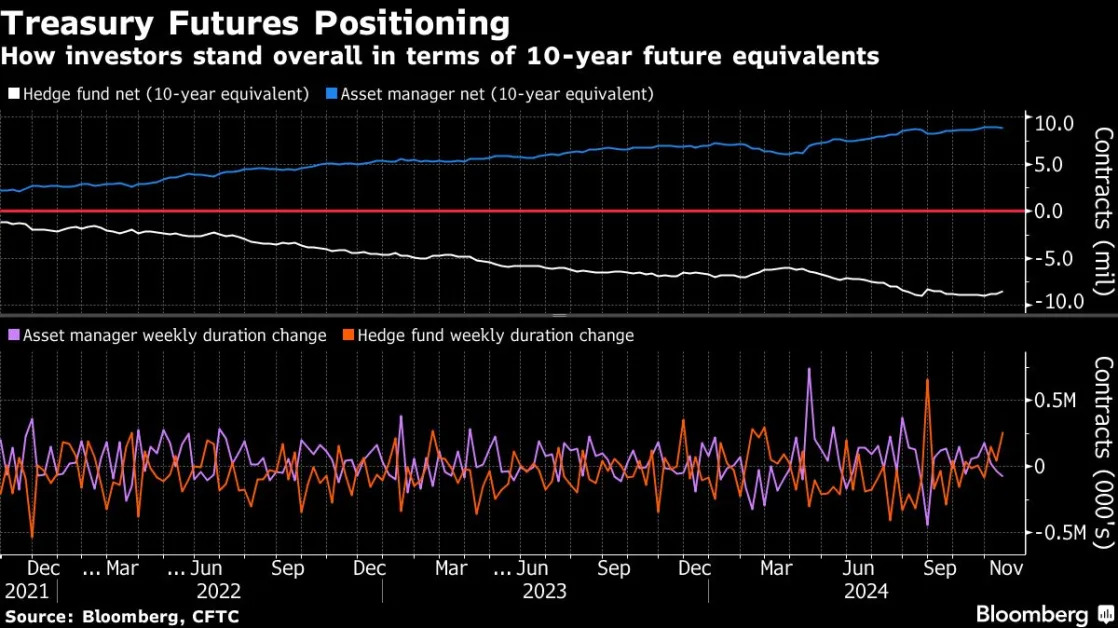

CFTC Futures Positioning

Asset managers unwound 72,000 10-year note futures equivalents to net long duration futures positioning in the week to Nov. 19, CFTC data shows. Over the same period hedge funds covered approximately 257,000 10-year note futures to net duration short across the Treasury futures strip. Over the week, hedge funds covered approximately $15.6 million per basis point in risk to net short positions in 2-year, 5-year and 10-year note contracts.