With 2025 on the horizon, investors are sharpening their focus on the year ahead, selecting portfolio additions that aim to bring solid returns.

“There is reason to be bullish,” says Jordan Jackson, a JPMorgan strategist covering the markets. He highlights positive trends in inflation and interest rates, noting that consumer spending is likely to respond in kind. “I think over the course of next year, we should continue to see consumers start to feel a little bit more confident about their wallet share and what they are able to spend,” Jackson added.

Meanwhile, the stock analysts at JPMorgan are starting to reveal their top picks for 2025 – stocks the bank’s experts expect to perform well in the coming year.

We’ve turned to the TipRanks database to pull up the details on two of their picks and have found that Wall Street shares an optimistic outlook, giving both names Strong Buy consensus ratings. Let’s take a closer look.

Vistra Energy ( VST )

First up is a utility-scale energy company, Vistra. This Texas-based electricity provider is the largest competitive power generation company currently working in the US market, with approximately 5 million customers and 41,000 megawatts of electric generation capacity. Vistra boasts a market cap over $48 billion, a workforce 6,800 strong, and a wide range of power facilities that includes gas, coal, nuclear, and solar generation capacities. In addition, Vistra has a strong commitment to producing zero-carbon power; its nuclear power generation capacity is the nation’s second-largest.

That nuclear power capacity is impressive, and Vistra has been working to expand it. In March of this year, Vistra completed an important acquisition move, adding 4 gigawatts of nuclear power from Energy Harbor to its portfolio, along with some 1 million customers. In addition, the company, in July, received approval from the Nuclear Regulatory Commission to keep its Comanche Peak nuclear plant in operation for another 20 years, through 2053.

Vistra isn’t just resting on its nuclear laurels. The company is also moving to expand its natural gas-fueled power production capabilities. It announced earlier this year an intention to increase ‘dispatchable, natural gas-fueled electricity capacity’ by more than 2,000 megawatts. The company already added more than 200 megawatts of upgrades during the second quarter of the year. The increase in gas-powered capacity is intended to improve Vistra’s grid reliability.

On the financial side, Vistra saw $6.28 billion in revenues during 3Q24,a figure that was up 54% year-over-year and beat the forecast by an impressive $1.27 billion. At the bottom line, the company realized $1.84 billion in net income. The company has a strong cash position, and generated $1.7 billion in cash from operations in the quarter.

Writing on Vistra for JPM, 5-star analyst Jeremy Tonet sees plenty of potential in the company, based on its strong production capacity. He says, “Top pick VST offers the optimal mix of all angles, in our view. We see very attractive upside from current levels, with a healthy step up in a blue sky scenario. In addition to nuclear upside, we see meaningful gas power leverage for VST, particularly as islanded gas in West TX (with the gas bottleneck wall moving east across TX) and Appalachia should support spark spreads, particularly given Permian electrification demand growth and a great call on gas due to PJM tightening.”

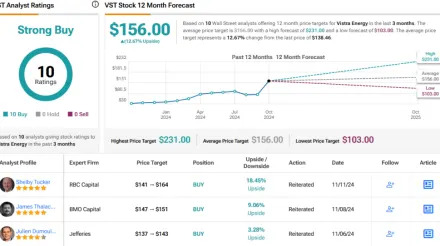

Quantifying this stance, Tonet puts an Overweight (i.e. Buy) rating on the stock, with a $178 price target that implies a 28.5% gain in the year ahead. (To watch Tonet’s track record, click here )

The Strong Buy consensus rating on Vistra is unanimous, based on 10 recent positive analyst reviews. The shares are trading for $138.46, and the $156 average price target suggests that the stock could see a one-year gain of nearly 12.5%. (See VST stock forecast )

EverQuote ( EVER )

The second stock we’ll look at is EverQuote, an online insurance marketplace. EverQuote’s platform connects the players in the insurance industry, allowing agents and agencies to publicize their offerings and buyers to browse, contact, and choose. The company’s umbrella covers most aspects of the insurance industry, including such major products as life insurance, car and vehicle insurance, and home and renter insurance.

The platform is designed to be intuitive and easy to use. Agents can post policies, along with pricing, and buyers can use search functions to locate insurance products and specific pricing points. These services are provided without charge; Everquote takes its own fees after policies are purchased, in the form of fees paid by the insurance policy issuers.

EverQuote is based in Cambridge, Massachusetts, where it was founded in 2011. Since then, the company has built up a market cap of $713 million. Last year, EverQuote brought in $287.92 million in total revenue – and the company has already surpassed that total by a wide margin this year.

That was clear from the Q3 financial results. EverQuote saw quarterly revenues of $144.54 million, beating the forecast by $4.19 million and growing by an impressive 162.8% from the prior-year period. The company realized a bottom line figure of 31 cents per share, or 10 cents per share better than had been expected. Looking ahead, EverQuote published Q4 revenue guidance in the range of $131 million to $136 million, which would mark year-over-year growth of 140% at the midpoint.

This stock is covered by JPM’s Cody Carpenter, who notes both the strong Q3 results and the solid prospects going forward, writing, “EVER reached record revenue and profit in 3Q, but expects healthy Auto carrier growth to continue in 2025 as more states re-open and carrier spend broadens. EVER shares have traded down 28% since 2Q earnings (vs. RTY +9%) on investor concern that the auto carrier recovery is mostly played out and uncertainty around the pending 1×1 consent rule, but we think the insurance cycle still has more room to run with impact from the 1×1 consent change manageable.”

Carpenter goes on to outline where he thinks this stock will go, adding, “We expect another year of outsized industry growth in 2025, and while the magnitude of beats/raises likely moderates going forward, we are still increasing our 2025/26 revenue by a healthy ~5% and our adj. EBITDA by 8%/13%, with our estimates above the Street’s. We reiterate our Overweight rating and EVER remains a top pick.”

The stated Overweight (i.e. Buy) rating is accompanied by a $28 price target that points toward a one-year upside potential of 49%. (To watch Carpenter’s track record, click here )

All in all, it’s clear that Wall Street agrees with Carpenter’s call on this. The stock has 6 recent analyst reviews on file, 5 Buys and a single Hold, making the consensus a Strong Buy. With an average price target of $31 and a current trading price of $18.81, this stock shows a one-year upside of 65% . (See EverQuote stock forecast )

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy , a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.