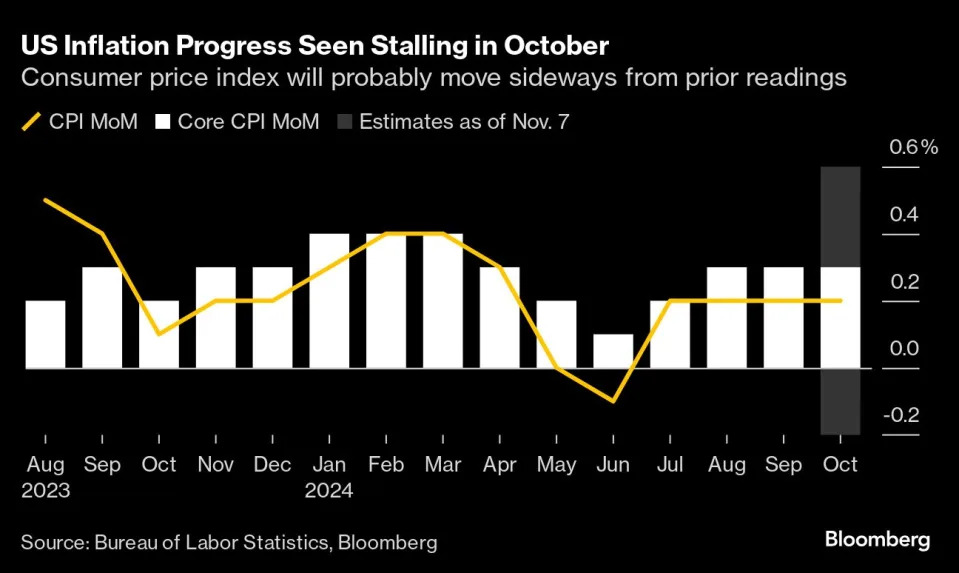

(Bloomberg) — US inflation probably moved sideways at best in October, highlighting the uneven path of easing price pressures in the home stretch toward the Federal Reserve’s target.

The core consumer price index due on Wednesday, which excludes food and energy, likely rose at the same pace on both a monthly and annual basis compared to September’s readings.

The overall CPI probably increased 0.2% for a fourth month, while the year-over-year measure is projected to have accelerated for the first time since March.

“The October CPI report will likely support the notion that the last mile of inflation’s journey back to target will be the hardest,” Wells Fargo & Co. economists Sarah House and Aubrey Woessner wrote in a report. “Excluding the more volatile energy and food components, the unwinding of pandemic-era price distortions has proven to be frustratingly slow.”

They added that prices of core goods probably rose again in October, due in part to higher demand for cars and auto parts after Hurricanes Helene and Milton. Evacuation orders from the storms also forced more people to stay in hotels, continuing what’s been a “glacial slowing” in services prices.

What Bloomberg Economics Says:

“We expect both CPI and PPI to come in hot, pushing long-end rates even higher — and further restraining the economy over the next couple months. We expect control-group retail sales to slow and the unemployment rate to continue to climb, reaching 4.5% by year end,”

—Anna Wong, Stuart Paul, Eliza Winger, Estelle Ou & Chris G. Collins.

Even so, “the story is very consistent, with inflation continuing to come down on a bumpy path,” and one or two bad reports won’t change that pattern, Fed Chair Jerome Powell said Thursday after the central bank cut interest rates by a quarter point.

The US government will also release wholesale inflation figures in the coming week, which probably picked up after stalling in September. Meantime, earnings growth that continues to outpace inflation likely contributed to another decent gain in retail sales, in data due Friday.

On Tuesday, Fed Governor Christopher Waller is due to speak at a banking conference before the central bank releases its latest Senior Loan Officer Opinion Survey. Powell is scheduled for an event later in the week, while New York Fed President John Williams and Dallas Fed President Lorie Logan are also on the calendar.

Minneapolis President Fed Neel Kashkari said on Sunday that the US economy has remained remarkably strong as the central bank progressed in beating back inflation, but the Fed is still “not all the way home.”

In Canada, meanwhile, home sales data for October will reveal whether the central bank’s rate cuts are starting to jolt the sluggish housing market.

A packed week for data elsewhere includes a range of economic numbers from China, wage and growth statistics in the UK, and multiple inflation readings, from India to Argentina. New European Union forecasts will also be published.

Asia

A data blast from China may show the economy’s performance improved marginally in October, with industrial output, fixed asset investment and retail sales all seen picking up a bit as the downturn in property investment moderates.

Even so, the data will underscore the necessity of the broad stimulus steps undertaken since late September as President Xi Jinping seeks to achieve his growth goals.

China’s slew of figures comes at the end of the week, on the same day that Japan is expected to report that its economic growth slowed to an annualized 0.6% quarter on quarter in the three months through September.

India’s inflation is projected to have picked up to 5.72% in October, while industrial output is seen rebounding in September in figures due on Tuesday.

Australia gets consumer and business confidence surveys on Tuesday before releasing a number of labor-market statistics later in the week.

The wage price index for the third quarter comes on Wednesday, and other employment statistics for October will be published a day later. Indonesia reports trade data on Friday.

Among central banks, the Bank of Japan releases a summary of opinions from its October meeting, when it held rates steady, and Reserve Bank of Australia Governor Michele Bullock appears on a panel on Thursday, with policymaking colleague Brad Jones doing the same a day later.

Europe, Middle East, Africa

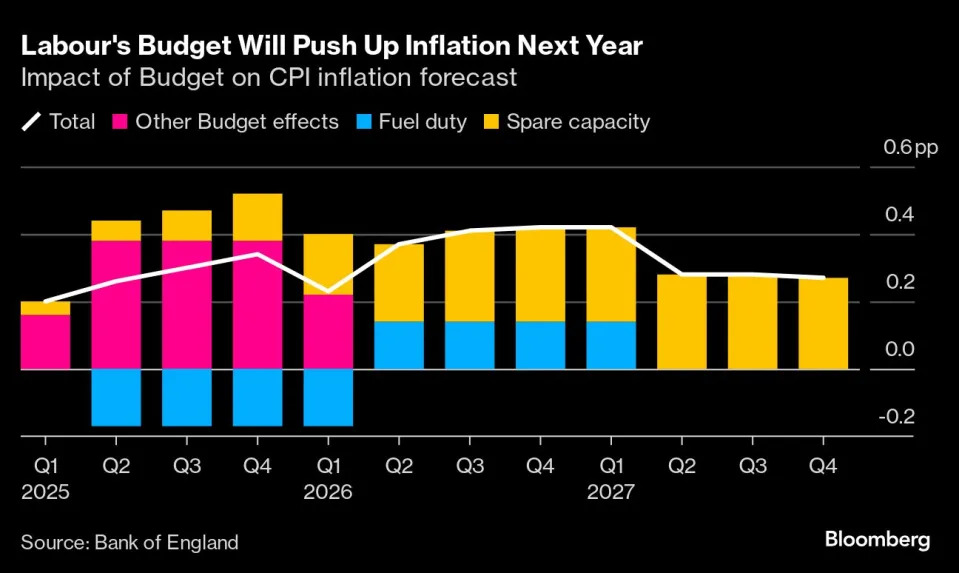

The UK will be in focus following Thursday’s Bank of England rate cut, which came with a warning of the inflationary impact of the recent budget. Governor Andrew Bailey is scheduled to make a speech on Thursday.

Wage numbers on Tuesday may show mildly slowing pay growth, offering limited reassurance to policymakers. A release on Friday will probably reveal economic growth to have weakened in the third quarter to 0.2% from 0.5% in the prior three months, according to economists.

Other countries with initial GDP numbers for the same period include Poland on Thursday and Switzerland on Friday.

Turning to the euro zone, Tuesday’s German ZEW index will offer a glimpse of investor sentiment at a time when Europe’s biggest economy is still struggling to shake off industrial malaise, and now faces the prospect of early elections as well.

Euro-zone industrial production on Wednesday will reveal the state of manufacturing at the end of the third quarter, and a second estimate of GDP will arrive concurrently. The European Commission in Brussels will release new economic forecasts for the region at the end of the week.

The European Central Bank on Thursday will publish an account of its October meeting, possibly containing hints on officials’ thinking for their December decision. Vice President Luis de Guindos, speaking in Madrid the same day, is among several officials scheduled to make appearances.

In an interview published Sunday, Robert Holzmann of Austria — one of the ECB’s more hawkish policymakers — said that a move next month is possibility but by no means guaranteed.

In Sweden, minutes of the Riksbank’s decision to ramp up easing with a half-point rate cut are due on Wednesday, followed by its financial stability report a day later.

In Russia on Wednesday, data will probably show the economy contracted in the third quarter — for the first time since war-related fiscal stimulus began boosting activity back in late 2022. Bloomberg Economics forecasts GDP to have fallen 0.3% to 0.5% in the three months through September.

Russia is among a number of countries releasing inflation data. Here’s an overview:

Meanwhile, Egyptian inflation data published Sunday showe the gauge slightly quickened for a third month, driven by a sharp rise in fuel prices.

Among central banks, monetary policymakers in Zambia are expected to leave their rate unchanged at 13.5% to support the drought-battered economy. That ordeal has prompted the International Monetary Fund to almost halve its 2024 growth projections, to 1.2%.

Latin America

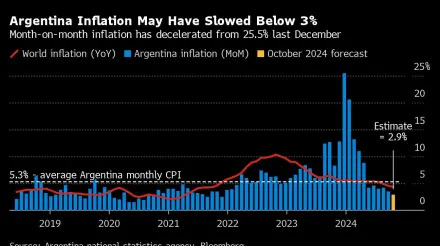

Argentina President Javier Milei is likely to get some welcome news with the October consumer prices report. Monthly inflation may have slowed to a three-year low of just under 3% with the annual reading coming in under 200%, down from April’s 289.4% peak.

Analysts expect a hawkish tone to the minutes of the Brazilian central bank’s Nov. 6 decision to hike to 11.25%. At the same time, forward guidance may be in short supply given that Brazil’s government had yet to commit to spending cuts, and all the wild cards inherent following the US election.

Economists expect a hike of at least the same magnitude at the BCB’s December meeting, and many have marked up their terminal rate projections to 13% or more.

Uruguay’s central bank has held its key rate at 8.5% since April and is likely to keep it there for a fifth straight meeting.

In Peru, Lima labor market figures and September GDP-proxy data are on tap, both underscoring the economy’s rebound from last year’s recession.

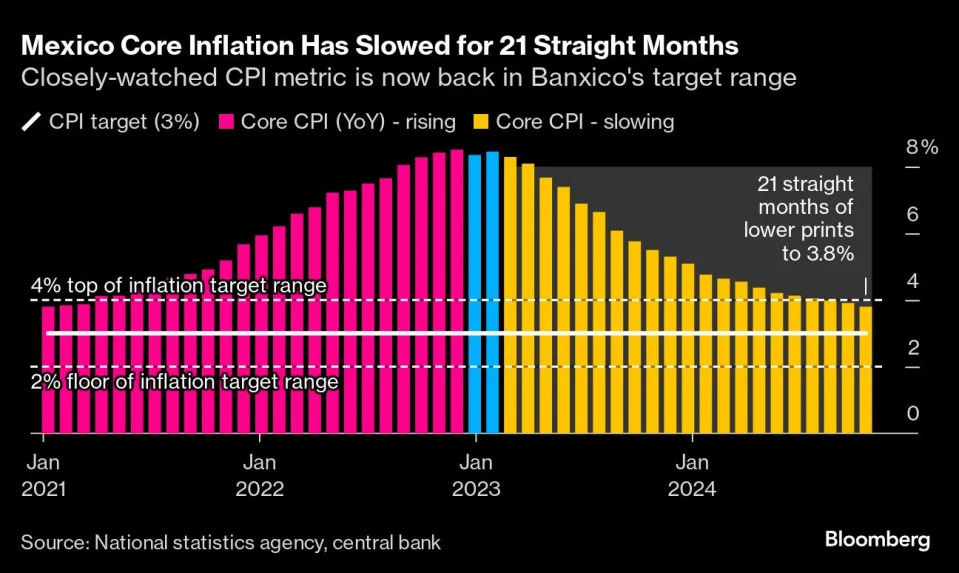

Banco de Mexico’s case for a third-straight rate cut on Nov. 14 looked pretty straightforward a month ago, but yet another bout of faster inflation makes it a slightly tougher call.

Still, the combination of slower growth and 21 straight months of slowing core inflation will likely see Governor Victoria Rodriguez and colleagues go ahead with the reduction to 10.25%.

—With assistance from Brian Fowler, Laura Dhillon Kane, Monique Vanek, Robert Jameson, Paul Wallace and Piotr Skolimowski.