There's no denying McDonald's is still the king of the restaurant business. Its 40,000 stores collectively did $119.8 billion worth of business last year, generating $25.5 billion of revenue and $8.5 billion of net income for the company. No other name even comes close to matching those numbers.

From an investor's standpoint, however, size isn't everything. Indeed, size can even be a drawback by virtue of making it tougher to tack on more growth. In some cases, a new McDonald's location's top competitor could be another nearby McDonald's restaurant that's already up and running.

If you're looking for a more promising bet from the quick-service restaurant space, consider Cava Group (NYSE: CAVA) instead.

What's Cava?

With only 323 restaurants as of the first quarter, Cava isn't exactly the household name that McDonald's is. In places where Cava's been operating for some time, though, consumers are in love with its Mediterranean fare. Its pita wraps and bowls are ideal for the fast-casual model while feeding the demand from evolving consumer preferences.

While the hamburger has dominated the quick-service restaurant landscape for decades, their health drawbacks are finally catching up with them. The enriched bread used to make most hamburger buns and heavily processed red meats are falling out of favor. Consumers are increasingly willing to pay even a small premium for fresh, natural ingredients like the ones Cava uses.

The real draw here, however, is the cuisine itself. It's relatively undiscovered by most U.S. consumers who are finding that, once they try it, they like it. Its health benefits are just an added marketability bonus.

In other words, this is the "something else" consumers appear to have been waiting for from the fast-casual restaurant industry.

Cava's got the results to prove it

And Cava's numbers back the claim up.

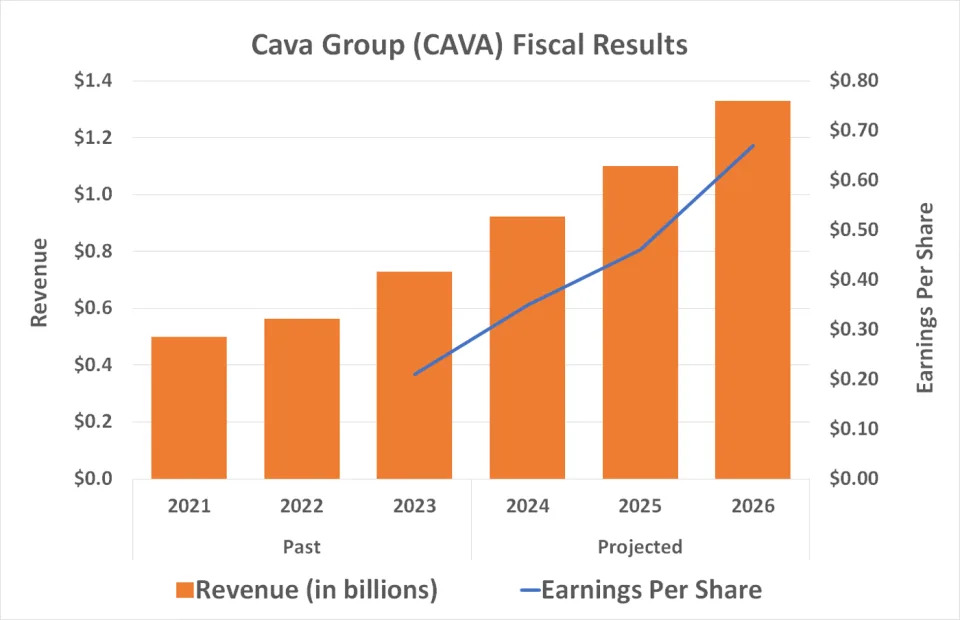

Take its first-quarter results as an example. During the three-month stretch ended April 21, Cava grew its top line 30.3% year over year to $256.3 million, while same-store sales improved 2.3% against a very tough comparison of 28.3% in the year-ago period.

Better still, despite its young age and small size, Cava Group is increasingly profitable. The first quarter's earnings before interest, taxes, depreciation, and amortization ( EBITDA ) of $33.3 million doubled year over year, and net income of $14.0 million completely reversed the year-ago loss of $2.1 million. Cava logged this profitability while opening 14 new restaurants during the quarter.

Overall, the first quarter's numbers extend existing trends that are expected to last at least through next year. In May, the company raised its full-year EBITDA outlook from a previous range of $86 million to $92 million to a revised range of $100 million to $105 million. Same-store sales growth forecasts were lifted, too. Analysts are also collectively calling for top-line growth of at least 20% this year and next year with per-share profits expected to more than double during that two-year span. It all points to one heck of a tailwind.

The kicker: Cava Group is essentially debt-free. As of April, its only long-term obligations to speak of were operating lease obligations mostly stemming from rents it's agreed to pay the landlords for its restaurant locations. As the numbers above show, though, Cava restaurants tend to operate profitably early on.

More important to interested investors, Cava enjoys the financial flexibility of not being beholden to bondholders who expect to receive regular interest payments whether or not paying them is in the organization's best interest at the time.

More reward than risk

So, is Cava a guaranteed winner? No, there's no such thing, especially in a business as fiercely competitive as the restaurant industry. The stock's also very expensive relative to its earnings. Young growth stocks tend to be uncomfortably volatile as well, and Cava Group is no exception.

Nevertheless, the potential reward here is more than worth the premium for risk-tolerant investors. There's a massive amount of room for Cava to continue expanding its footprint for years to come and many reasons to believe it will be able to do so.

Before you buy stock in Cava Group, consider this: