SentinelOne (NYSE: S) stock recorded impressive gains of 45% since the beginning of June, which should come as a relief to shareholders. The cybersecurity specialist endured a difficult start to 2024 and was down substantially in the first five months of the year.

Its recovery is remarkable considering that investors pressed the panic button following the release of the company's fiscal 2025 first-quarter results three months ago. The reason behind that sell-off was reduced full-year guidance. However, savvy investors started buying SentinelOne stock following its sell-off.

That turned out to be a prescient strategy. SentinelOne stock received a nice shot in the arm after a CrowdStrike software update crashed a vast number of global IT systems on July 19. Now, it looks like SentinelOne's business may be benefiting in the aftermath of CrowdStrike's blunder, as its latest results beat Wall Street's expectations and the company raised its full-year guidance.

Let's take a closer look at SentinelOne's latest quarterly report and consider why the stock could deliver more upside.

SentinelOne's solid results point toward robust demand for its cybersecurity offerings

On Aug. 27, SentinelOne released its results for its fiscal 2025 second quarter, which ended July 31. The company's revenue rose 33% year over year to $199 million, exceeding the consensus estimate of $197.3 million. What's more, it swung to an adjusted profit of $0.01 per share from a loss of $0.08 per share in the same quarter last year. Analysts had been expecting SentinelOne to break even on the bottom line.

Those stronger-than-expected results can be attributed to an improvement in the customer base, as well as SentinelOne's ability to drive stronger spending from its existing customer base. This was evident from management's comments in the latest shareholder report:

Our customer growth in Q2 was broad-based across businesses of all sizes and geographies. Our momentum with large enterprises remains strong, as our customers with ARR of $100,000 or more grew 24% y/y to 1,233. Customers with more than $1 million in ARR grew even faster, reaching another company record.

SentinelOne points out that its ARR, or annualized recurring revenue, measures its ability to acquire new subscription customers and also maintain or expand its relationships with existing customers. The metric refers to the annualized revenue run rate of the subscription and consumption and usage-based agreements in force at the end of the period.

So, the 32% growth in SentinelOne's ARR in its second quarter to $806 million indicates that its future revenue pipeline is improving. As a result, the company set its full-year revenue guidance at $815 million. In May, it issues fiscal 2025 revenue guidance to a range of $808 million to $815 million, citing macroeconomic challenges.

Though SentinelOne management says that the macroeconomic uncertainty still persists, "the performance shortcomings of other market offerings are becoming visible to the public." Management didn't mention CrowdStrike by name, but it did address the "latest global IT outage," describing it as "an avoidable incident that was born out of risk-prone software deployment practices and a fragile product architecture."

So, there's a possibility of SentinelOne witnessing an increase in demand for its products thanks to CrowdStrike's problems. And, as it attracts more customers thanks to others' missteps and wins a bigger share of the cybersecurity spending of its existing customers, it could witness further margin improvements. It is worth noting that the company's non- GAAP operating margin was negative 3% in fiscal Q2 compared to negative 22% in the prior-year period.

In addition, its adjusted gross margin improved by 3 percentage points year over year to 80% last quarter. So, SentinelOne's bottom line still has a lot of room for growth, which is precisely the reason why analysts are expecting its earnings growth to take off.

Solid bottom-line growth could lead to more stock upside

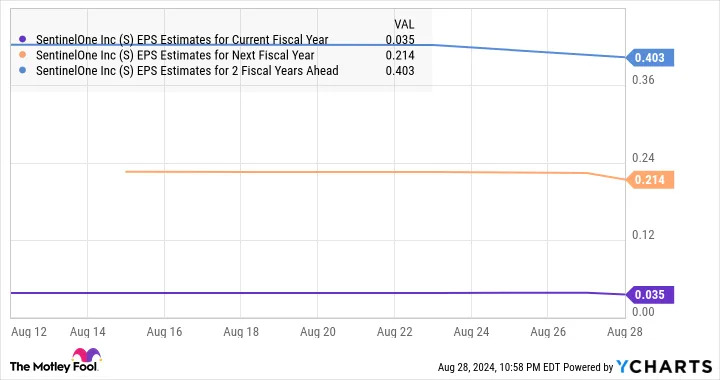

We have already seen that SentinelOne posted an adjusted profit in its fiscal 2025 Q2, as compared to a loss in the same period last year. The company finished its fiscal 2024 with a loss of $0.28 per share, which was a massive improvement over the $0.70 per share loss it reported in its fiscal 2023. The company is expected to get in the black this year and follow that with two solid years of bottom-line growth.

What's more, analysts are expecting SentinelOne's earnings to increase at a compound annual rate of 40% for the next five years. All this indicates that this cybersecurity stock may be able to sustain its impressive rally not only in the near term but also in the long run. That's why it may be a good idea to buy SentinelOne now, while it is trading at 10 times sales. That's a small premium to the U.S. technology sector's average sales multiple of 8, and one that it seems capable of justifying thanks to its impressive growth.

Before you buy stock in SentinelOne, consider this: