By any reasonable measure, Palantir (NYSE: PLTR) is succeeding. The company has one of the best artificial intelligence (AI) software application platforms out there and is a top pick for integrating AI models within a business to drive decisions. This dominance has caused its revenue growth to accelerate each quarter, making the stock popular among AI investors.

But there is one factor -- Palantir's steep valuation -- that some investors fail to consider. And investors should weigh that valuation very closely, particularly when considering a new investment in this dynamic company.

Palantir's business is knocking it out of the park

Palantir has been in the AI software market for longer than much of its competition, which is likely why it's succeeding. Originally, Palantir's software was for government use and was deployed to intelligence agencies as well as battlefield command to ensure that those making decisions had the best information in front of them.

Eventually, management saw a use for this software outside of government, so it expanded to the civilian side. While government revenue still makes up over half of Palantir's total, the commercial side is growing quickly.

The growth from the commercial side centers around the "unprecedented demand" (management's words) for its Artificial Intelligence Platform (AIP). AIP allows its customers to integrate AI (including large language models) throughout a business, giving them the ability to automate processes like never before, incorporating human approval if necessary.

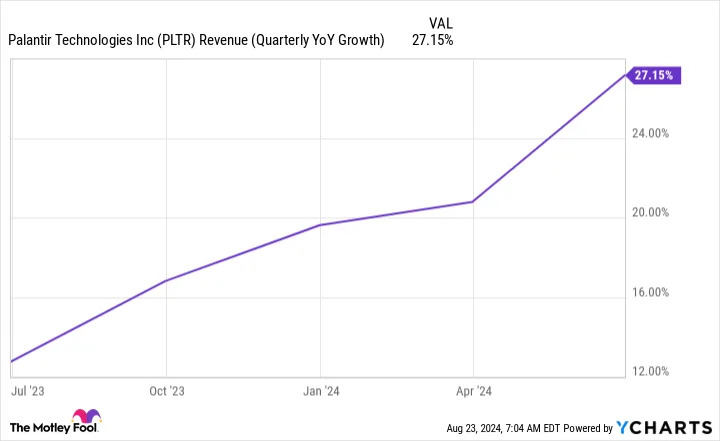

The possibilities of AIP are truly endless, and the growth has been impressive, especially in the U.S. In the second quarter, U.S. commercial revenue was Palantir's fastest-growing segment, up 55% year over year to $159 million. Still, Palantir's other segments didn't do too badly, with overall commercial revenue increasing 33% year over year and government sales rising 23%. Overall, this led to a growth rate of 27%, which continues the trend of accelerating revenue growth.

Revenue growth is great, but accelerating revenue growth is better. Another plus for Palantir is that it's a profitable company. In Q2, it delivered a profit margin of 20% -- a company record .

Palantir is doing everything necessary to be a successful company and then some, so it's no wonder that many investors are excited about it.

However, the stock has an Achilles' heel that everyone should know about.

The expectations attached to the stock are extreme

Everything I wrote about above is well known in the market. As a result, the stock has gotten incredibly expensive.

Ninety times forward earnings and 31 times sales are incredibly high valuations. While Palantir is growing fast, these kinds of prices are usually reserved for companies that double or triple their revenue quarter after quarter. Palantir isn't doing that, which concerns me.

Let's say Palantir's growth rate accelerates even more to 30% year-over-year growth and maintains that figure for five years. That would give Palantir $9.2 billion in annual revenue by 2029. If its profit margins improve to 25%, that would equate to $2.3 billion in profits.

Dividing that figure by Palantir's current market cap would yield its price-to-2029-earnings ratio, which is 31 times forward earnings.

So for Palantir to return to a valuation level similar to that of other established software companies, it must improve its margins to 25% and grow at a sustained 30% pace. That's a very tall task, and I don't think Palantir can live up to it.

As a result, I think the price is far too high for the stock, so I'm going to avoid it. Palantir will continue to succeed as a business , but the growth expectations baked into the stock are too much for my taste.

Before you buy stock in Palantir Technologies, consider this: