NextEra Energy Partners (NYSE: NEP) currently offers a monster dividend yield. The renewable energy company's payout yields more than 14% , which is about 10 times higher than the S&P 500 's dividend yield. Further, the company plans to continue growing its payout in the future.

However, as attractive as this renewable energy dividend stock might seem, those seeking a sustainable income stream should forget about it right now . Instead, income-focused investors should buy Brookfield Renewable (NYSE: BEPC) (NYSE: BEP) . While it offers a lower yield (over 5%), it's on a much more sustainable foundation.

Running low on power

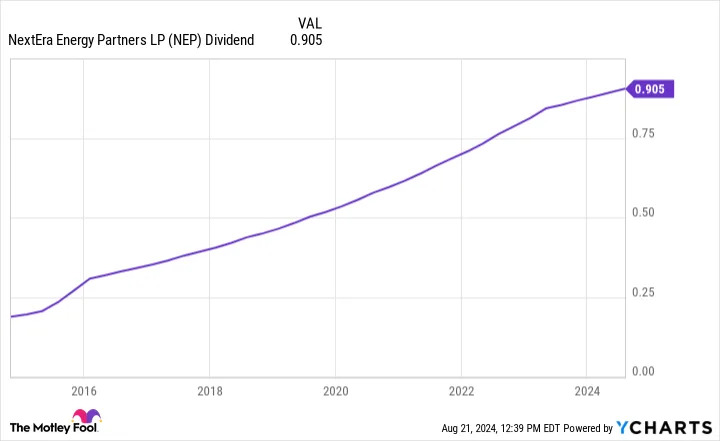

NextEra Energy Partners currently has a terrific record of paying dividends. The renewable power producer has increased its payout every single quarter since it came public over a decade ago.

The company expects that steady upward trend to continue. It plans to increase its payment by 5% to 8% per year through 2026, with a target of 6% annually. While that is a much slower pace than initially expected (12% to 15% annually), it's a solid rate, especially for such a high-yielding dividend stock .

NextEra Energy Partners had to tap on the brakes with its growth plans due to its surging cost of capital . Rising interest rates and its plummeting stock price have made it too expensive to borrow money to refinance maturing funding and finance new acquisitions at attractive rates due to its junk -rated credit. That forced the company to pivot is strategy. It's selling its natural gas pipeline operations to cover its upcoming funding buyouts. It's also relying on organic expansion projects (primarily wind repowering projects) to boost its cash flow in support of its dividend growth plan.

The company expects its dividend payout ratio will be in the mid-90% range through 2026, which is way too high. Because of that, there's a high risk that the company will need to cut its payout in the coming years . That makes it too risky for income-seeking investors right now.

Ample power to continue growing

Brookfield Renewable's financial profile is on a much more sustainable foundation these days . Unlike NextEra Energy Partners, Brookfield Renewable has a strong investment-grade credit rating. Meanwhile, the company doesn't rely on short-term financing to fund acquisitions. It primarily uses equity and low-cost, long-term, fixed-rate debt. Because of that, higher interest rates haven't had any impact on its growth strategy.

Instead of tapping the brakes, Brookfield Renewable has stomped on the accelerator. The company expects to grow its funds from operations (FFO) per share at a more than 10% annual rate through at least 2028. It sees several factors driving its growth, including inflation-linked contractual rate increases, margin enhancement activities, its development pipeline, and acquisitions.

Whereas NextEra Energy Partners has primarily relied on acquisitions to power its growth (mainly drop-down transactions from its parent, NextEra Energy ), Brookfield focuses on higher-return organic development projects. The company has a massive backlog of projects that should power its growth for years to come .

Meanwhile, the company has a much different acquisition funding strategy: capital recycling . Brookfield routinely sells mature assets to fund higher-returning new investments. For example, the company expects to generate $1.3 billion from capital recycling activities this year, which will help it fund the $970 million it has committed to invest across several accretive acquisitions.

Brookfield expects its growing cash flows to support 5% to 9% annual dividend growth, which aligns with its expected 6% to 9% organic growth rate. That would continue its trend of increasing its payout by at least 5% per year, something it has accomplished for 13 straight years. Meanwhile, with earnings growing faster than its dividend, Brookfield's payout ratio will steadily decline from its already comfy sub-75% level.

A much more sustainable income stream

NextEra Energy Partners' double-digit dividend yield might seem alluring. However, that payout isn't on a solid foundation these days due to its weak financial profile. Because of that, income-focused investors should forget about it until the company fixes its issues.

They should buy Brookfield Renewable instead. The company has a long history of growing its high-yielding payout, which should continue. It backs its dividend with a much stronger financial profile and highly visible growth prospects. Because of that, it offers a much more sustainable income stream that should steadily rise in the future.

Before you buy stock in NextEra Energy Partners, consider this: