Shares of cosmetics company e.l.f. Beauty (NYSE: ELF) have quickly plunged about 26% from recent highs and it's because the growth rate has suddenly come crashing down for this high-growth business.

On Aug. 8, e.l.f. Beauty's management actually raised its full-year revenue guidance. Previously, it had expected net sales of $1.23 billion, at most, for its fiscal 2025 (which ends in March 2025). Now it expects net sales of $1.28 billion, at least, which is an improvement. But investors reacted negatively nevertheless because of what this guidance implies: a dramatic drop in its sales growth rate .

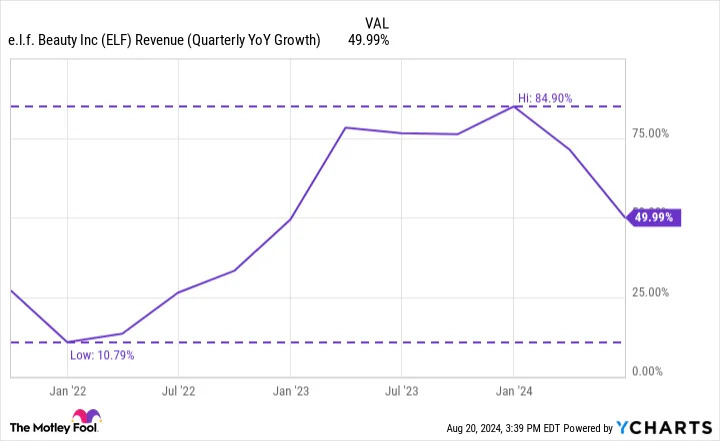

For fiscal 2025, e.l.f. Beauty's updated guidance implies 25% to 27% top-line year-over-year growth. But consider that first-quarter net sales were up by 50%. This means that the final three quarters of fiscal 2025 are only expected to grow 20% from the same three quarters of fiscal 2024.

As the chart below shows, e.l.f. Beauty's shareholders haven't experienced growth this slow since early 2022.

What should investors do now that e.l.f. Beauty's growth rate has plunged?

This is a great business

The cosmetics space is competitive, but e.l.f. Beauty has been able to take market share at a strong pace in recent years. One possible reason for this may be its price point. Management says that its prices are around $6 on average whereas competitors' are up closer to $9. And lower prices encourage users to experiment with the brand.

Being a low-cost leader is usually fraught with challenges. Consequently, investors might expect razor-thin margins from e.l.f Beauty. But nothing could be further from the truth. As its revenue has exploded higher in recent years, its gross margin has risen to a high 71% and its operating margin is a strong 12%.

Being a low-cost leader and a high-margin business is rare and it's a great reason to like e.l.f. Beauty.

Another intriguing aspect of e.l.f. Beauty's business is international penetration. According to management, many of the company's rivals derive more than 70% of sales from international markets. By comparison, only 16% of e.l.f. Beauty's sales are outside of the U.S., pointing to a strong, long-term growth opportunity.

What to do with e.l.f. Beauty stock

Successful investors understand that stocks are more than just ticker symbols -- they represent ownership stakes in real businesses. But another important truth is that the business is not the stock. What I mean is, recognizing a good business is an essential skill. But recognizing a timely investment opportunity is another crucial ability.

This is why Warren Buffett says, "It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price." In one sentence, Buffett acknowledges both business quality and investment timeliness.

I've already highlighted why e.l.f. Beauty is a high-quality business. But because growth was so strong for so long, it seems investors sent the stock up to an unreasonably expensive price, not the fair one that Buffett would look for. As the chart below shows, its price-to-sales (P/S) valuation is about twice as expensive as what it was prior to its dramatic surge in revenue growth.

Since the growth rate is dropping back down, it wouldn't be surprising for e.l.f. Beauty stock to drop back down to a more normalized valuation. That would suggest some further downside ahead. For this reason, I don't necessarily believe e.l.f. Beauty stock is a timely opportunity even though it's pulled back 26% already.

That said, a stock's valuation is nearly impossible to predict. Any number of things could excite investors and send the valuation higher. The opposite is also true. This is why investors should focus on the business over the valuation, generally speaking.

For e.l.f. Beauty's shareholders, I think the choice is easy: If you're comfortable with the possibility of it dropping more with slowing growth in the near term, it's likely good to keep holding for the long term. It's a great business and international expansion can really sustain top-line growth for a long time.

For those looking to buy e.l.f. Beauty stock today, it's important to recognize that its valuation is expensive. And this may necessitate a longer-than-normal holding period to enjoy positive returns.

For investors who struggle with downside potential and longer holding periods, it's probably best to wait to see if the valuation for e.l.f. Beauty stock drops down to more normal levels before buying. But for those who can be patient, buying e.l.f. Beauty stock in small chunks over time may be one way to approach this promising beauty company.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »