Pharmacy chain Walgreens Boots Alliance (NASDAQ:WBA) reported Q1 CY2025 results beating Wall Street’s revenue expectations , with sales up 4.1% year on year to $38.59 billion. Its non-GAAP profit of $0.63 per share was 21% above analysts’ consensus estimates.

Is now the time to buy Walgreens? Find out in our full research report .

Walgreens (WBA) Q1 CY2025 Highlights:

Company Overview

Primarily offering prescription medicine, health, and beauty products, Walgreens Boots Alliance (NASDAQ:WBA) is a pharmacy chain formed through the 2014 major merger of American company Walgreens and European company Alliance Boots.

General Merchandise Retail

General merchandise retailers–also called broadline retailers–know you’re busy and don’t want to drive around wasting time and gas, so they offer a one-stop shop. Convenience is the name of the game, so these stores may sell clothing in one section, toys in another, and home decor in a third. This concept has evolved over time from department stores to more niche concepts targeting bargain hunters or young adults, and e-commerce has forced these retailers to be extra sharp in their value propositions to consumers, whether that’s unique product or competitive prices.

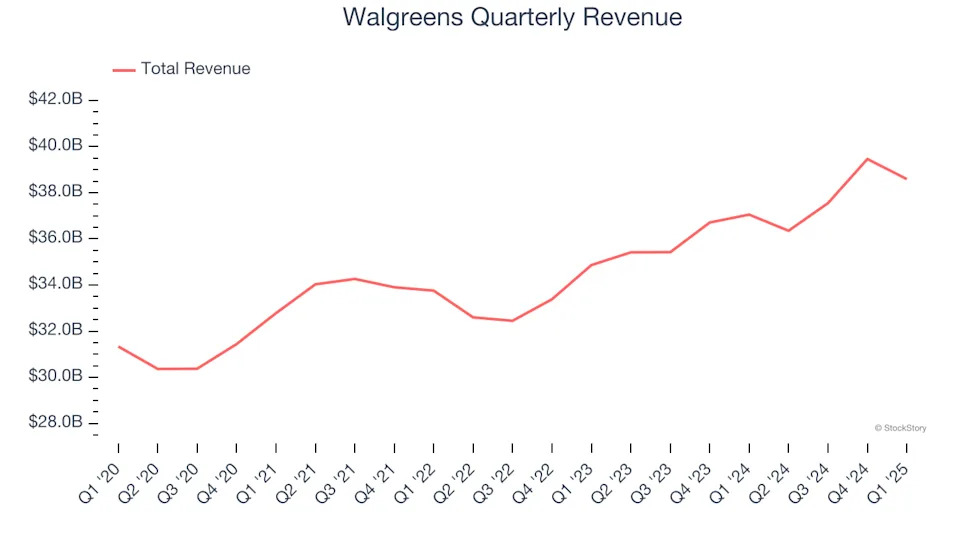

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years.

With $151.9 billion in revenue over the past 12 months, Walgreens is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. For Walgreens to boost its sales, it likely needs to adjust its prices or lean into foreign markets.

As you can see below, Walgreens grew its sales at a sluggish 2.9% compounded annual growth rate over the last six years (we compare to 2019 to normalize for COVID-19 impacts). This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, Walgreens reported modest year-on-year revenue growth of 4.1% but beat Wall Street’s estimates by 2.2%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a slight deceleration versus the last six years. This projection doesn't excite us and indicates its products will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. .

Same-Store Sales

Walgreens has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing locations. On average, the company has posted exceptional year-on-year same-store sales growth of 6.6%.

Note that Walgreens reports its same-store sales intermittently, so some data points are missing in the chart below.

Key Takeaways from Walgreens’s Q1 Results

Given the pending transaction, pursuant to which WBA will be acquired by entities affiliated with Sycamore Partners, the company is withdrawing fiscal 2025 guidance. As for the quarter, we enjoyed seeing Walgreens beat analysts’ revenue and EPS expectations this quarter. Overall, this quarter was solid. The stock traded up 1.1% to $10.85 immediately after reporting.

Is Walgreens an attractive investment opportunity right now? We think that the latest quarter is just one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .