While inflation has eased to 2.9% in July, interest rates remain elevated, with the Federal Reserve’s key rate currently at 5.25% to 5.50%. However, it is widely expected that the Fed will begin cutting rates as early as next month.

A reduction in rates is likely to send ripples across various sectors, with the biotech industry being particularly affected. Biotech companies, which often operate with significant overhead costs, are especially sensitive to changes in interest rates. But with a rate cut likely in the offing, market dynamics for biotech could see a favorable shift in the coming months.

However, regardless of the Fed’s next move, Jefferies analyst Michael Yee suggests that the biotech sector’s financial health is more robust than it might seem.

“As we pass Q2, our updated EV/ cash tracker shows SMid Biotech (up to $5B cap) is attractive and cheap… The cash position for biotech remains solid with near $200M in median cash balances and a median runway of >2 years and higher than historical average — given lots of cash raised in the last 12 months of follow-ons… The sector is healthy and well financed with a median of 2.3 years of cash to support key data readouts,” Yee opined.

Building on this, Jefferies analyst Maury Raycroft is pounding the table on two biotech stocks in particular, arguing they are well-positioned to deliver strong returns in the year ahead – in one case, as much as 270%.

Using the TipRanks database , we’ve looked up the big-picture view on both of these picks and it looks like the rest of the Street agrees with the Jefferies take – both are rated Strong Buys by the analyst consensus. Let’s see why they are drawing plaudits across the board.

Inozyme Pharma (INZY)

The first Jefferies pick we’ll look at is Inozyme Pharma, a clinical-stage biotech company focused on addressing three severe and rare diseases affecting the skeletal system, vascular system, and soft tissues. These conditions are linked by a common underlying issue: disorders in the body’s bone mineralization process. When this process goes awry, it can lead to chronic, irreversible, and debilitating illnesses. In response, Inozyme has developed an innovative therapeutic agent, INZ-701, which has demonstrated efficacy in treating mineralization disorders caused by deficiencies in the ENPP1 and ABCC6 genes.

The company currently has three clinical trial programs underway for INZ-701, with the most advanced focusing on treating ENPP1 deficiency. Inozyme expects to complete enrollment for ENERGY-3, a pivotal Phase 3 pediatric trial for this indication, within this quarter, with topline data expected in the second half of 2025. Due to the significant increases in PPi levels (the primary endpoint) observed in the adult ENPP1 deficiency trial, ENERGY-3 is considered a de-risked study. In addition, Inozyme plans to release data from ENERGY-1, a Phase 1b trial involving infants with ENPP1 deficiency, in Q4 2024.

INZ-701 is also being developed to treat ABCC6 deficiency, a genetic condition that causes the calcification disorder Pseudoxanthoma elasticum (PXE). Following positive topline data from an ongoing Phase 1/2 trial involving 10 adult participants, the FDA granted the company Fast Track Designation in July. Meanwhile, preparations are underway for a Phase 3 trial in pediatric patients with ABCC6 deficiency, which is anticipated to commence in Q1 2025, pending FDA approval.

But that’s not all – Inozyme is also exploring INZ-701’s potential to offer therapeutic benefits to patients with calciphylaxis as a result of end-stage kidney disease (ESKD). The company has initiated the SEAPORT-1 Phase 1 trial to assess the safety, tolerability, pharmacokinetics, and pharmacodynamics of INZ-701 in ESKD patients undergoing hemodialysis, with interim data expected in Q4 2024.

For Jefferies analyst Maury Raycroft, all of this points toward a bullish future for Inozyme. He sums up the near-term potentialities of the INZ-701 programs for investors, writing: “We think [Inozyme’s] market cap reflects the ENPP1 deficiency opportunity with little value ascribed for PXE ($900M peak revenue), and we expect regulatory alignment on a pediatric pivotal in the fall of 2024 to be a key catalyst (stock +30%/-10%). We think calciphylaxis opportunity represents another $1B in revenue that could be derisked with ph.I interim data in 4Q (stock+20%/-10%), which is not priced into the stock… INYZ’s ‘701 increased critical biomarker PPi into a similar range as healthy volunteers in 2 ph.I/IIs in adults w/ ENPP1 deficiency and PXE, which we think de-risks all 3 clinical programs.”

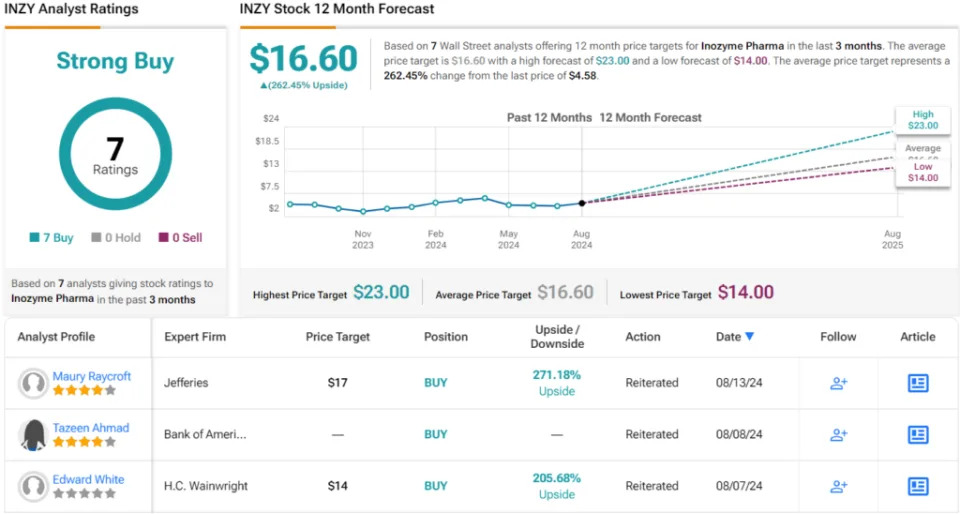

In line with his optimistic take, Raycroft rates INZY shares a Buy, along with a $17 price target. Should the target be met, a twelve-month gain of 271% could be in store. (To watch Raycroft’s track record, click here )

Wall Street’s analysts can be a contentious lot – but when they agree on a stock, it’s a positive sign for investors to take note. That’s the case with INZY, as all 7 recent analyst reviews on the stock are Buy recommendations, making the consensus rating a unanimous Strong Buy. Currently trading at $4.58, the stock has an average price target of $16.60, suggesting a potential 262% gain over the next year. (See INZY stock forecast )

Tango Therapeutics (TNGX)

Next up is Tango Therapeutics, a biotech firm dedicated to improving treatments in the field of oncology. Tango is working on the discovery and development of novel drug agents, capable of precisely targeting cancer tumors. The company is researching areas such as tumor suppression genes and how they influence the ability of cancer cells to evade immune cell agents.

Specifically, Tango has developed a synthetic PRMT5 targeting program. PRMT5 is a crucial gene for cell survival, making it an attractive target in cancer treatment. However, conventional non-synthetic PRMT5 inhibitors have posed significant risks, as they can be harmful to normal cells, particularly bone marrow cells, in addition to cancerous ones. A synthetic PRMT5 inhibitor, therefore, represents a potentially groundbreaking advancement in oncology.

Tango believes it can achieve this goal with its lead candidates, TNG908 and TNG462, both currently in clinical trials. TNG908, an MTA-cooperative PRMT5 inhibitor capable of penetrating the blood-brain barrier, is in the dose expansion phase of a Phase 1/2 trial. This trial focuses on patients with MTAP-deleted solid tumors, including non-small cell lung cancer, pancreatic cancer, and glioblastomas – tumors that exhibit MTAP deletions, which are present in 10% to 15% of all human cancers, with an even higher prevalence in glioblastomas.

The second candidate, TNG462, is poised to be a best-in-class MTA-cooperative PRMT5 inhibitor. It is also in a Phase 1/2 trial, currently testing two dose levels against various cancers, including non-small cell lung cancer, pancreatic cancer, bladder cancer, sarcoma, mesothelioma, and cholangiocarcinoma. Tango anticipates releasing a comprehensive clinical data update for both PRMT5 inhibitors later this year.

Analyst Raycroft, in his coverage for Jefferies, is impressed by Tango’s having ‘Two differentiated assets in the MTAP space,’ as well as by the upcoming data catalysts. He says of the company, “We believe TNGX’s market opportunity is underestimated based on unique positioning. ‘908 could gain significant market share in GBM given strong unmet need (25% pts survive 1yr with SOC). ‘462 could gain more market share vs competitors if it can demonstrate a better efficacy/safety profile (as preclinical data suggests).”

Looking ahead, Raycroft sees Tango’s clinical programs as being relatively de-risked compared to typical Phase 1 oncology programs, noting, “PRMT5 is a well understood epigenetic target that leads to MTAP-del cell death. We think PRMT5-MTA inhibition could result in ≥30% ORR in some tumors, where histologyagnostic approval is a potential upside scenario.”

Summing up, the analyst rates TNGX as a Buy, with a $19 price target that indicates potential for a 91% upside for the year ahead.

Are other analysts in agreement? They are. Only Buy ratings, 5 to be exact, have been issued in the last three months. Therefore, the message is clear: TNGX is a Strong Buy. Given the $14 average price target, shares could soar 40.5% in the next year. (See TGTX stock forecast )

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy , a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.