(Bloomberg) -- How soon do they start, how fast do they go and where do they end?

Federal Reserve officials are largely in agreement it’s almost time to lower interest rates. Investors are onside, too, with markets fully pricing in a quarter-point cut when the Federal Open Market Committee meets next month.

But plenty of tension awaits in the coming months as US monetary policy approaches a critical turning point. Fed Chair Jerome Powell and his colleagues are now steering between two opposing sets of risks. While seeking to finish off the threat from inflation, they’ll want to lower borrowing costs at just the right time and speed to prevent a swift deterioration in the labor market.

“They are thinking not about the first two rate cuts but the whole strategy over the next six to nine months,” said Derek Tang, an economist at LH Meyer/Monetary Policy Analytics. “They’re asking: Where do we want to be if shocks come our way?”

That suggests a strategy of risk-management, an approach central banks frequently turn to during times of high uncertainty. In other words, they look at their two goals and ask where the greater risk lies. Then they’ll lean against that risk while keeping an eye on the other.

FOMC Divisions

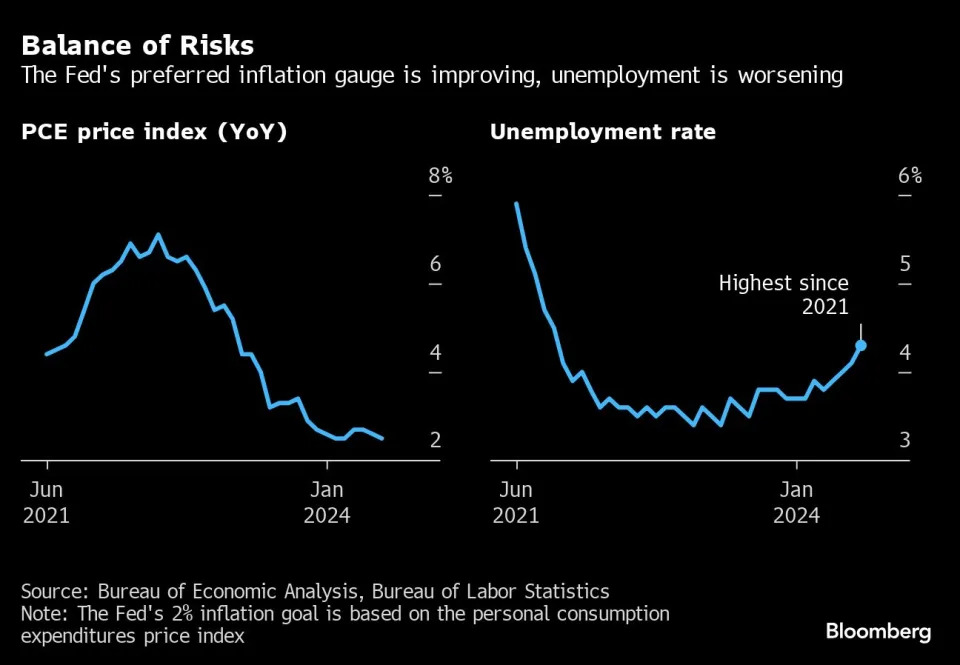

It’s never easy. As inflation has declined, that has pushed real rates higher even as the Fed has held its benchmark rate steady in a range of 5.25% to 5.5% for more than a year. Job creation is slowing, inflation has cooled and Powell has a committee that is split over where they see the most risk.

Fed Governor Michelle Bowman and Atlanta Fed President Raphael Bostic are in the camp asking, what’s the hurry? They want to see more proof that price stability is in hand and still detect signs of resilience in the labor market. Some of the rise in unemployment, they point out, is due to job-seekers coming off the sidelines. Moreover, while companies have slowed hiring, they haven’t ramped up layoffs.

To this group, Powell can point to the July consumer inflation report to make the case that a quarter-point cut in September is unlikely to stoke price increases. Excluding food and energy, the consumer price index rose 0.2% in the month, and the three-month annualized figure, a signal of the near-term trend, advanced 1.6%, the lowest since February 2021.

There’s also a group of officials who’ve painted something of a red line above the current unemployment rate of 4.3%.

“We have now confirmed that the labor market is slowing, and it is extremely important that we not let it slow so much that it tips itself into a downturn,” San Francisco Fed President Mary Daly said Aug. 5.

The stakes are enormous. The US economy has seen clear benefits from a tight labor market in recent years. It pulled many people into the workforce and raised pay, helping to defend pocketbooks against inflation.

But that could turn quickly, and the rise in the jobless rate from 3.7% in January to 4.3% in July hinted at what’s to come if the economy slows too much. Wage growth has slowed, and Black and Latino unemployment rates have drifted higher from the end of last year. That’s true for those without a college education as well.

“The FOMC has deliberately been slowing the pace of growth to let off the excess pressure in the economy,” said David Wilcox, the Fed’s former chief forecaster who is now director of US economic research at Bloomberg Economics. “It is in that circumstance of sluggish growth that this fragility comes to the surface.”

Securing a soft landing is a high priority for Powell, a matter that could determine his personal legacy. It is, he acknowledged last month, what’s keeping him up at night.

The credibility of the US central bank is also in play. Powell and his colleagues were late to respond to the spike in inflation after first calling it “transitory.” Tipping the economy into a recession by holding rates too high for too long — in effect, missing on the back end, as well — would certainly anger both parties in Congress and shape public sentiment.

That damage would come just as former President Donald Trump and his running mate, JD Vance, sense the time is right to open a debate about the Fed’s role. Both have said politicians should have a greater say on monetary policy.

Risk Management

Powell has already hinted he’ll take a risk-management approach to help him navigate the coming months. In considering the consequences of getting it wrong in either direction, history shows the darker scenario likely lies on the employment side. With the exception of the pandemic, recent recessions have had deep and long-lasting impacts on the labor market, especially for the lowest income workers, as people drop out of the workforce — some of them permanently.

With that in mind, the Fed may not only communicate a path for interest rates back to some equilibrium or neutral level for the economy but also one that seeks to offset those higher-cost risks. Markets are already hedging against that possibility, pricing in close to a full percentage point in cuts by year end.

“The predominant risk at this point is that the softening in the labor market gains momentum and the economy tips into an unnecessary and unwanted recession,” Wilcox said. “A 50-basis-point cut ought to be the base case for their first move. The labor market doesn’t need to soften any more.”