After a slight market sell-off, plenty of companies look like great deals. Most of the news causing this decline will be irrelevant in three to five years, so there's no reason to panic.

At the top of my shopping list today are Taiwan Semiconductor Manufacturing (NYSE: TSM) , Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL) , and Amazon (NASDAQ: AMZN) . All three companies have fantastic long-term tailwinds and look like strong buys right now.

Taiwan Semiconductor

Taiwan Semi is probably the most critical company in the world. Without its manufacturing capabilities, companies like Apple , Nvidia , and almost every other company that depends on high-tech devices would be out of luck. Its best-in-class semiconductor manufacturing capabilities allow it to produce cutting-edge chips in the 3nm marketing category.

These specialized production techniques require unbelievable knowledge and skill to be implemented at a large scale, so unseating TSMC is nearly impossible, although there are still worthy competitors out there.

Right now, the stock is about 10% off its 2024 highs, but it's still worth a buy even though investors have missed the true bottom. At 26 times forward earnings, it still isn't expensive for the growth it's putting up.

In the second quarter, revenue grew 33% in U.S. dollars while providing solid guidance for the third quarter (32% revenue growth). Taiwan Semi is well-positioned to benefit from the steady increase of technology in our lives. If investors have the chance to buy the stock on sale, they should take the opportunity.

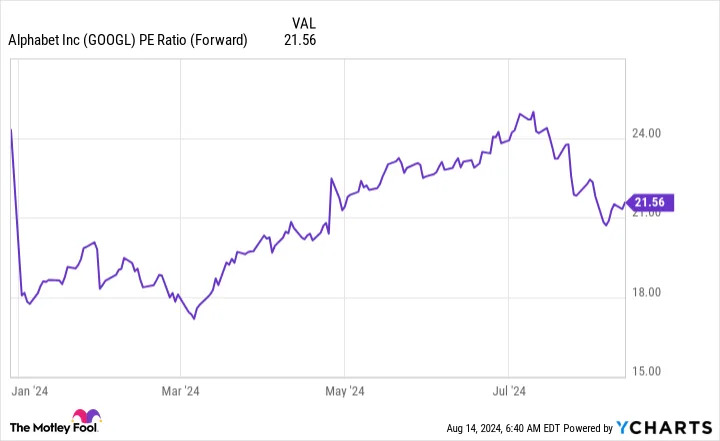

Alphabet

Even without the sell-off, Alphabet looked like a prime buying opportunity. Despite being one of the largest companies in the world, Alphabet doesn't earn a premium valuation like its peers. The parent company of Google, YouTube, and the Android operating system only carries a price tag of 22 times earnings.

Considering that its peers have valuations of 30 times forward earnings or greater, Alphabet looks like one of the cheapest big tech stocks. And its cheapness isn't associated with its business performance, because Alphabet has been crushing it.

In Q2, Alphabet's revenue rose 14% year over year and increased its operating margin by three percentage points. Google Cloud, in particular, had a great quarter, with revenue rising 29%. This is a critical division, and strong results show that it is still a top pick in the cloud computing space.

Alphabet is a dominant company that doesn't have the premium that its peers carry. This is an excellent opportunity to scoop up shares for a fantastic price.

Amazon

In some investors' eyes, Amazon may be doing the worst out of these three. In Q2, sales only rose 10% to $148 billion, but investors wanted more. The company also issued guidance for 8% to 11% revenue growth for Q3, which also didn't please the crowd.

However, that's the wrong figure to be looking at. Amazon isn't going to provide lightning-fast growth due to its sheer size. Instead, I'd point investors to how profitable Amazon is becoming. Amazon offers operating income guidance, which is projected to come in between $11.5 billion and $15 billion in the next quarter, compared to $11.2 billion in the year-ago period.

Unless operating income comes in on the very bottom end of management's guidance, that will provide excellent earnings growth, which is critical in bringing down Amazon's valuation.

36 times forward earnings isn't necessarily cheap, but getting Amazon to maximum profitability in one year also isn't a realistic expectation. Amazon's long-term trajectory is to grow its earnings much faster than revenue as it works to increase profitability across the board.

This is my primary investment thesis in Amazon, and it will take years to play out. If investors focus on revenue growth and are selling off the stock as a result, then that provides a cheaper buying price for me.

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this: