Even the best growth stocks see their shares pull back. But just because their share price is down, that does not necessarily mean that the stocks are down and out for good. In fact, Amazon famously lost 90% of its value over a two-year period back in the early 2000s, only to become the nearly $2 trillion company it is today.

Let's look at three consumer good growth stocks that are down but certainly not out.

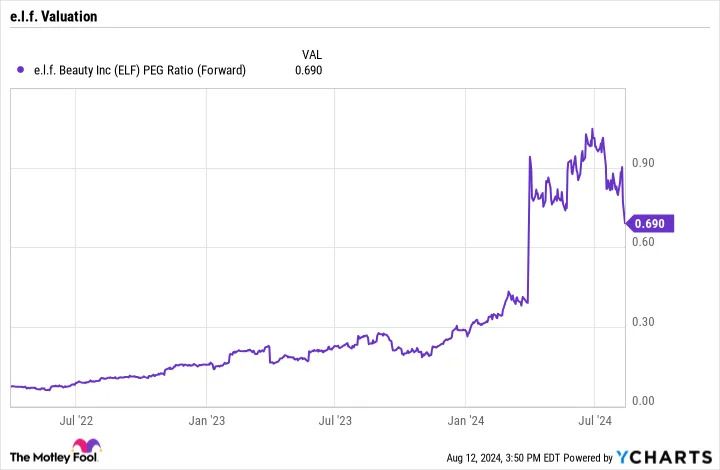

1. e.l.f. Beauty

Off nearly 30% from its recent high, e.l.f. Beauty (NYSE: ELF) remains one of the best growth stories in the consumer goods space. Through the use of influencers and by making close copies of popular prestige cosmetic products, the company has been able to gain shelf space and take a huge share in the mass-market cosmetic category. In fact, it has become the No. 1 cosmetic brand among teens, according to consumer surveys.

While growth may slow from the breakneck pace it's had the past couple of years, e.l.f. still has a long pathway of growth in front of it. It's made strong initial inroads with expanding internationally, but it is still only in a few markets. The company has over-indexed with the Hispanic community in the U.S., so Latin America could be a big future opportunity.

Meanwhile, the company has just recently gotten into skin care. With only a 2% market share in skin care in the U.S., the potential to take share in this category is a huge opportunity. Given the company's performance in the cosmetics space over the past few years, there is no reason to believe it won't have the same success in skin care.

Trading at a price/earnings-to-growth ratio (PEG ratio) of under 0.7, this growth stock is very attractively priced after its recent sell-off. A PEG under 1 times is generally considered attractive, but for a growth stock, it squarely places e.l.f. in the bargain bin.

2. Nike

After reporting only a 1% increase in revenue on a constant currency basis for its fiscal 2024, which ended in May, and guiding for a mid-single-digit sales decline in fiscal 2025, it may be best to call Nike (NYSE: NKE) a former growth stock. After all, it hasn't been showing much growth lately.

However, following the stock's most-recent sell-off, investors can buy the iconic brand at one of the cheapest valuations it has been at in a long time at an under 20 P/E ratio.

But let's not count out Nike just yet. One of the best ways for a management team to get a stock back on track is to give extremely conservative guidance and then sprint and jump over the low bar that has been set. Nike looks poised to do just that.

One reason why is that the company should see an Olympic boost, with it spending more around the event than anytime in the past. Nike also launched a number of new products centered around the event.

Research outfit Similarweb, meanwhile, showed that Nike's strategy was paying off with a huge spike in visits to its website and solid conversions to sales. In China, which has been a trouble spot, the company has seen a jump in sales for customized T-shirts of women's gold medal tennis player Zheng Qinwen, who it sponsors.

Given its valuation and low expectations, now could be the time to "just do it" and add Nike to your portfolio as it looks to return to being a growth company.

3. Dutch Bros

Shares of Dutch Bros (NYSE: BROS) got crushed after the coffeehouse operator told investors that new store openings this year would come in at the lower end of its guidance as it looked to optimize its real estate strategy. However, the long-term prospects for the company remain in place, as it has a long runway of expansion opportunities ahead of it.

The company's store format is on the small side, typically ranging from 800 square feet to 1,000 square feet, with multiple drive-thru lanes and a pick-up window. This small format allows for a relatively inexpensive buildout program while creating solid throughput, as evidenced by its $2.0 million average unit volume (AUV), which measures the average sales of its stores.

With only 912 locations at the end of Q2 (612 of them company-owned), the popular coffee chain that started out in Oregon is still predominantly in the western U.S. although it does have some locations in places like Florida, Kentucky, and Tennessee. This makes it a nice regional-to-national expansion story.

The company is also just beginning initiatives like mobile orders, which should be a nice boost to sales. This also shows that the company is still in the early days of benefiting from technological improvements that many other chains have already implemented. This creates future growth opportunities.

Dutch Bros trades at a similar forward price-to-sales (P/S) multiple as rival Starbucks but should show a lot more growth, given that it is still in the early days of expansion. Due to this, I would be a buyer of the stock on the recent weakness.

Before you buy stock in Nike, consider this: