(Bloomberg) — Greed has overcome fear on Wall Street — and the market cataclysm that shook up the world in recent weeks may well prove a mere blip on long-term price charts.

Yet the summer rout will also go down as a particularly extreme example of a trend that’s shaped modern finance for years now: Increasingly frequent shocks blowing up with little warning.

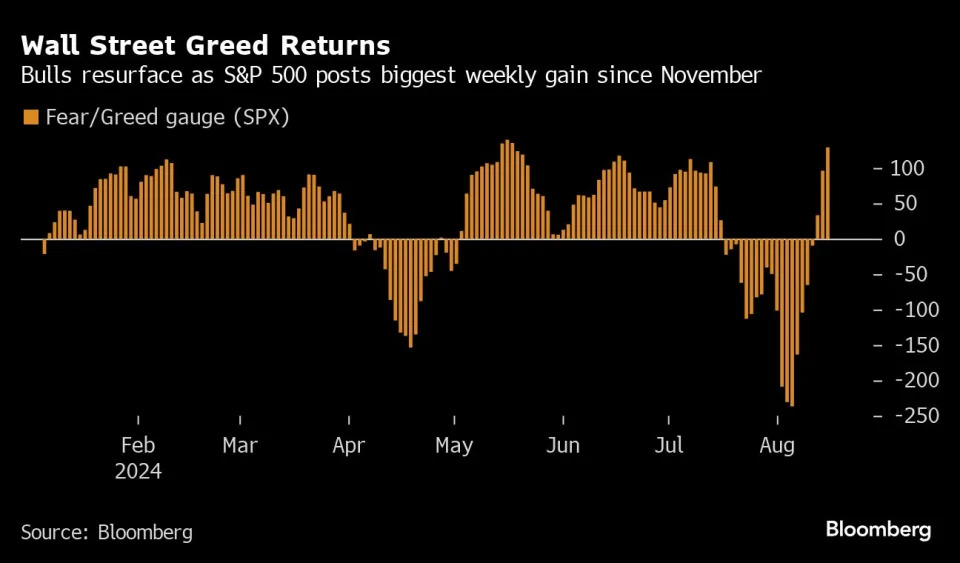

As fast as volatility erupted, it has calmed, with the S&P 500 posting its biggest weekly gain since November, junk bonds scoring a week of gains and Treasury yields stabilizing. In one especially vivid example, the VIX Index, Wall Street’s “fear gauge,” has just broken two records: the fastest-ever spike of 25 points or more, and the fastest comeback from the spike, according to UBS Group AG.

The reversals are a nightmare for anyone trying to attach sensible explanations to the motion of markets. Was the trigger for the August swoon technical in nature, or something more sinister like fear of a Federal Reserve policy failure and an oncoming AI bust? Whatever your view, febrile markets are periodically moving from euphoria to despair — and back again just as fast — amid an interconnected herd of leveraged traders.

Indeed, the increasing frequency of fast-reversing price spasms has been an expanding wing of financial research since at least 2019, when Bank of America Corp. strategists used the term “fragility” to describe events that have become five times more common than in the previous century. They include the 2015 China devaluation scare, 2018’s Volmageddon trauma and the Covid crash.

“We would characterize the extreme market ups and downs over the past couple of weeks as the latest illustration of how markets have become inherently more fragile in the past 15 years,” said Nitin Saksena, the head of US equity derivatives research at BofA. “The speed with which the shock dissipated only adds to our conviction, as fast-mean reversion is a hallmark of fragility shocks due to their technical nature. A more fundamental shock would have more staying power.”

Past blowups have included crowded trades and dicey liquidity, both of which were in evidence in 2024, when a handful of artificial-intelligence-fueled super stocks dominated index returns and left large swaths of the equity universe all but unloved. Fragility became evident when the swift unwinding in popular positions, which also included the yen carry trade, rapidly spread across borders and morphed into market-wide disruptions.

That such disparate assets got caught up in the tumult adds to Saksena’s view that something in the nature of markets themselves contributed. Bitcoin, the Swiss franc, investment-grade credit, copper, Japan’s Nikkei 225 all took lumps, he notes, a lesson in “how pervasive fragility is across markets and how dysfunctional markets can become in times of stress due to extreme supply/demand imbalances.”

A slew of systematic funds sharply reduced their exposure to stocks last week, and quants that chase market trades were squeezed out. By some estimates, three-quarters of the global carry trade was unwound by last Wednesday, only for corporate clients and hedge funds to rush back days later.

“We had a unique set of circumstances where a combination of positioning, pricing of risk, the level of volatility and market liquidity all lined up in a way where you challenged the things that had been working all year round,” said Ashish Shah, chief investment officer of public investing at Goldman Sachs Asset Management. “And you really took down the positioning around those themes.”

This week subsequently delivered the biggest concerted rally of 2024 with stocks, bonds, credit rising in tandem, according to Bloomberg-compiled data tracking popular ETFs. The S&P 500 scored its best weekly gain for the year of 3.9%, snapping a four-week losing streak. The world’s largest Treasury exchange-traded fund rallied about 1% as investment-grade and junk bonds scored similar wins. Gold climbed to $2,500 for the first time. The VIX dropped below 15 after rising above 65 at the height of the maelstrom.

A raft of recent data prompted traders to recalibrate their Fed bets after comforting signals on inflation. The producer price index, for example, rose less than forecast earlier in the week. Swap traders are still pricing nearly a percentage point of Fed easing in 2024, with the market gearing up for a first reduction in September. Attention shifts to the Jackson Hole symposium for any hints on how Chair Jerome Powell is viewing the economy.

“We went from being solely focused on Fed and rates and inflation and now it’s all about the earnings and the economic slowdown and volatility,” Katerina Simonetti, senior vice president at Morgan Stanley Wealth Management, said on Bloomberg TV. “It’s very confusing for investors who tend to have sometimes a bit of a short-term memory.”

While the bond market continues to flash warnings of economic weakness, all 11 main equity sectors staged a concerted rally this week. With the Fed all set to cut interest rates into a still-expanding economy, investors are back to worrying about missing a rally in riskier corners — and have been unwinding the hedges they bought just weeks ago.

With sentiment potentially moving back toward euphoric levels ahead, there’s a greater chance for another disorderly market event. Framed this way, a cohort of investing professionals — particularly those that offer portfolio insurance known as tail-risk hedging — argue that markets are ever-more fragile. Thank investor herding, questionable liquidity — and the rise of volatility-sensitive investors who buy and sell on technical, rather than economic, triggers.

“We’re in this zone of constantly making new highs, similar to how we were around any other market tops,” said Josh Kutin, head of asset allocation, North America at Columbia Threadneedle Investments. “That makes for a more fragile market. It creates an atmosphere where people are more easily spooked.”

—With assistance from Lisa Abramowicz.