Last week’s spate of market volatility, the poor July jobs report, and the prospect of Federal Reserve interest rate cuts are together prompting renewed fears of a near-term recession. A recent contraction in the PMI – purchasing managers’ index – hasn’t helped matters. And while the market is bouncing back this week, investors are starting to diversify their portfolios – and are looking for a slightly more defensive stance.

The packaged food industry makes a sound place to look for such portfolio diversity. Food is one of those necessary products that tend to prove recession-proof – and packaged food stocks saw gains during the period of COVID lockdown policies. While the packaged food industry is subject to its own cycles and headwinds, it can usually be relied on for long-term staying power.

These facts underlie a recent report from Leah Jordan, who covers the American food industry for Goldman Sachs.

“We believe food-at-home spending should continue to grow at +LSD with balanced support from volume and pricing/mix due to a solid consumer cash flow backdrop. That said, category exposure is key in this normalized environment as both ends of the spectrum–value and premium–continue to gain share. As a result, we favor companies with lower exposure to private label risk as well as greater organic growth opportunities through a differentiated portfolio in alignment with key consumption trends (e.g., convenience, health/wellness, flavor diversity),” Jordan opined.

Looking ahead, Jordan goes on to make some specific stock picks, naming two packaged food stocks in particular as ‘top buy’ propositions in today’s conditions. We’ve used the TipRanks database to find out what the broader view is of these two stocks. Let’s take a closer look.

Conagra Brands (CAG)

The first packaged food stock we’ll look at is Conagra, a Chicago-based holding company with a rich history dating back to 1919. Originally founded as a milling company, Conagra has grown into a food industry powerhouse with an extensive portfolio that spans everything from snacks and everyday staples to healthier alternatives. Last year, Conagra generated around $12.3 billion in revenue. The company relocated its headquarters to Chicago in 2016, employs over 18,000 people, and operates 42 manufacturing and packaging facilities across the US, Canada, and Mexico

In an interesting announcement, Conagra made public earlier this month the acquisition of Sweetwood Smoke & Co., known as the producer of FATTY Smoked Meat Sticks. This deserves some note as Conagra already owns the Slim Jim brand of meat sticks – a snack brand known for its low-end image. The acquisition of FATTY points toward a move to a higher-end snack line-up. The financial arrangements of the deal were not disclosed.

Also of note, especially for defensive-minded investors, Conagra in July declared a dividend of 35 cents per common share. This is in-line with the previous quarter’s dividend and marks the fifth consecutive quarter at this rate. The dividend is scheduled for payout on August 29, and the $1.40 annualized rate gives an inflation-beating forward yield of 4.7%.

Turning to financial results, we find that Conagra reported its earnings for fiscal 4Q24 on July 11 – and showed a top line of $2.9 billion. This reflected a year-over-year decline of 2.3% in net sales, and missed the forecast by $20 million. At the bottom line, Conagra reported an EPS of 61 cents by non-GAAP measures. This was 4 cents better than had been anticipated.

So Conagra is a soundly positioned company with a strong place in a defensive stock niche – and Goldman’s Leah Jordan describes the shares as a ‘top idea.’ She writes of this food giant, “We view CAG as having a well positioned frozen and snack portfolio that aligns with current convenience and consumption trends, which should support better than feared results, along with an attractive valuation, noting it has the highest FCF yield in our coverage.”

Getting into greater detail, Jordan goes on to explain why Conagra has been slipping under investors’ radar recently, adding, “Since the current management team came to CAG nine years ago, they have repositioned the company through an overhaul of its processes and culture while revitalizing its brand portfolio, noting the biggest change came when it acquired Pinnacle Foods in 2018. As the transition largely unfolded in the shadow of Covid with dynamic shifts in food-at-home demand and inflation, we think this has been underappreciated by investors.”

These comments back up Jordan’s Buy rating on Conagra shares, while her $36 price target implies that a one-year gain of 16.5% lies ahead for this stock. (To watch Jordan’s track record, click here )

The Goldman view is more bullish than the Street’s consensus on this stock. CAG shares have a Hold consensus rating, based on 13 recent reviews that include 2 Buys to 11 Holds. The shares are priced at $30.82 and their $30.54 average target price suggests they will stay rangebound for the time being. (See Conagra stock forecast )

Mondelez International (MDLZ)

Next up on today’s list of Goldman Sachs’ food stock picks is Mondelez International, another major player based in Chicago. Mondelez emerged as a spin-off from the iconic Kraft Foods, which separated its snack businesses from its grocery operations back in 2012. As the inheritor of the snack division, Mondelez now boasts a portfolio that includes household names like Ritz crackers, Triscuit, Philadelphia cream cheese, and Chips Ahoy cookies. With products available worldwide, Mondelez raked in over $36 billion in total sales last year.

Employing around 91,000 people, Mondelez prides itself on a diverse workforce that drives innovation in its product development. The company operates in over 80 countries, maintaining a vast network of factories, distribution centers, research and development facilities, and administrative offices.

Financially, Mondelez reported $8.34 billion in net revenues for Q2 2024, as disclosed on July 30. This figure fell short of estimates by $110 million and represented a nearly 2% decline year-over-year. However, despite those misses, the company’s bottom line, with a non-GAAP EPS of $0.86, exceeded forecasts by 7 cents per share. Additionally, Mondelez’s management anticipates organic net revenue growth at the upper end of the 3% to 5% range for the full year 2024 and projects generating over $3.5 billion in free cash flow.

It’s worth noting that despite these strong fundamentals, MDLZ shares have underperformed the broader market this year, dipping slightly by 0.5% year-to-date, while the S&P 500 has risen by 14%.

Mondelez has a commitment to cash returns for investors, and in the first half of this year, the company met that commitment to the tune of $2.2 billion. The returns were made in both stock repurchases and in dividend payments. In a positive sign for return-minded investors, the company on July 30 announced an upcoming dividend payment increase of 11%, to a new payment of 47 cents per common share. This will give a new annualized payment of $1.88 with a forward yield of 2.7%. The new dividend will be paid out on October 14 of this year.

For Goldman Sachs, the key point here is quality. As analyst Jordan writes, “We view MDLZ as a high-quality core holding that should generate above-average earnings growth within our coverage, supported by its portfolio of organic opportunities and emerging market exposure.”

Jordan goes on to explain why the stock’s recent losses should not deter investors, adding, “We believe recent stock underperformance has been tied to ongoing market share losses and increased pricing action needed for its US biscuits business along with uncertainty around elevated cocoa cost pressure, although we note sequentially improving trends for both metrics recently while the company has also taken proactive steps to address the issues.”

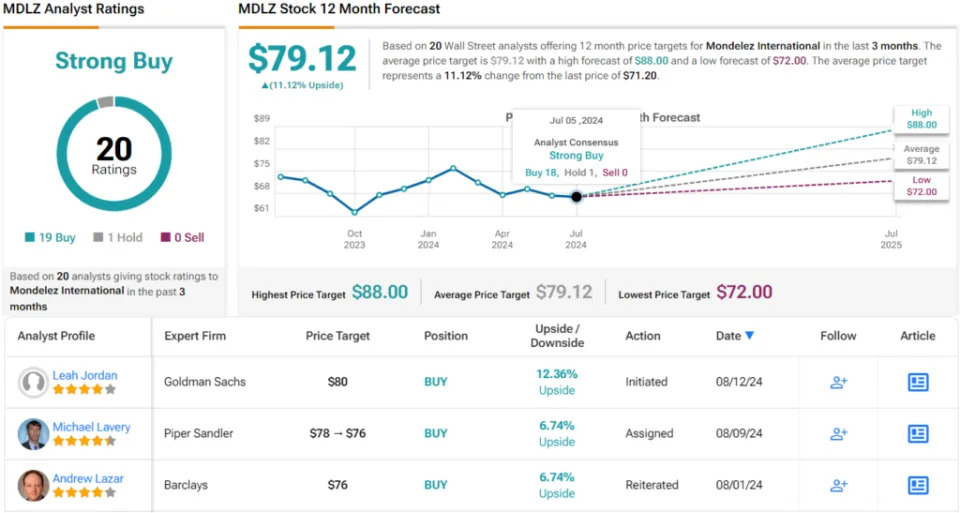

For Jordan, MDLZ shares merit a Buy rating, and her price target, now set at $80, points toward a one-year upside potential of 11.5%.

All in all, Mondelez shares have picked up 20 recent analyst reviews – and the lopsided split of 19 Buys to 1 Hold gives the stock its Strong Buy consensus. The stock is selling for $71.20 and has an average price target of $79.12, implying a gain of 11% by this time next year. (See MDLZ stock forecast )

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy , a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.