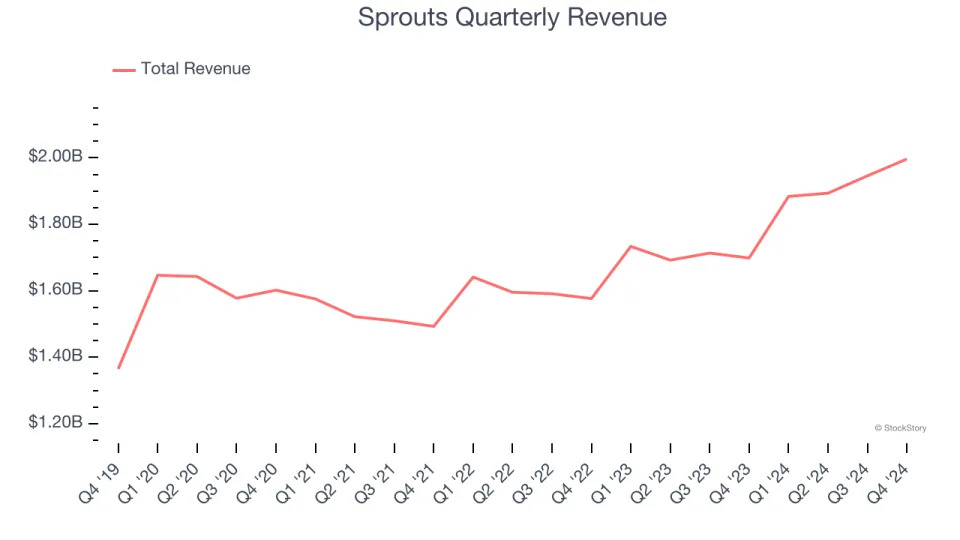

Grocery store chain Sprouts Farmers Market (NASDAQ:SFM) reported Q4 CY2024 results beating Wall Street’s revenue expectations , with sales up 17.5% year on year to $2.00 billion. Its non-GAAP profit of $0.79 per share was 7.5% above analysts’ consensus estimates.

Is now the time to buy Sprouts? Find out in our full research report .

Sprouts (SFM) Q4 CY2024 Highlights:

“2024 was a remarkable year for our company,” said Jack Sinclair, chief executive officer of Sprouts Farmers Market.

Company Overview

Playing on the secular trend of healthier living, Sprouts Farmers Market (NASDAQ:SFM) is a grocery store chain emphasizing natural and organic products.

Grocery Store

Grocery stores are non-discretionary because they sell food, an essential staple for life (maybe not that ice cream?). Selling food, however, is a notoriously tough business as grocers must deal with the costs of procuring and transporting oftentimes perishable products. Plus, the costs of operating stores to sell everything from raw meat to ice cream and fresh fruit are high. Competition is also fierce because grocers and other peers such as wholesale clubs tend to sell very similar brands and products. On the bright side, grocery is one of the least penetrated categories in e-commerce because customers prefer to buy their food in person. Still, the online threat exists and will likely increase over time rather than dwindle.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $7.72 billion in revenue over the past 12 months, Sprouts is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Sprouts grew its sales at a tepid 6.5% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts), but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, Sprouts reported year-on-year revenue growth of 17.5%, and its $2.00 billion of revenue exceeded Wall Street’s estimates by 1.7%.

Looking ahead, sell-side analysts expect revenue to grow 10.4% over the next 12 months, an acceleration versus the last five years. This projection is eye-popping and indicates its newer products will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. .

Store Performance

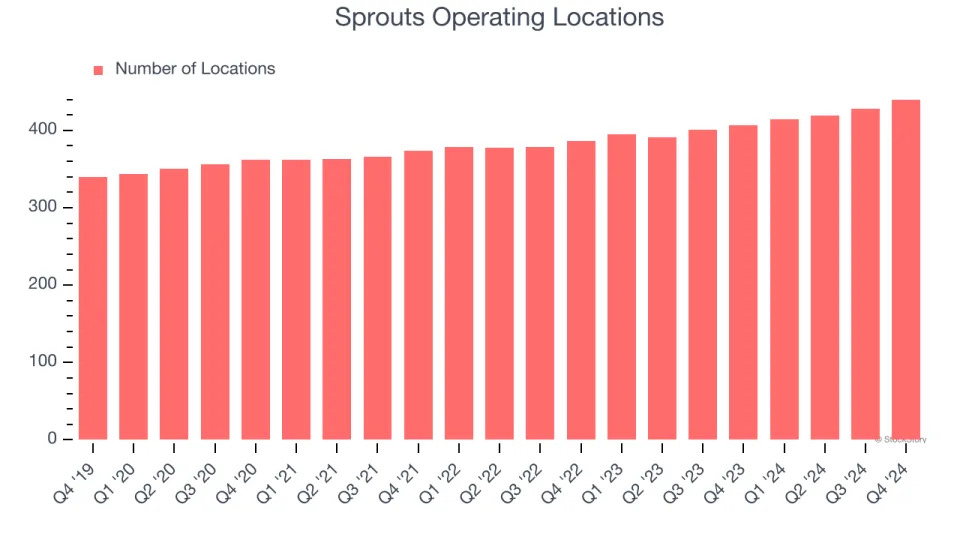

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Sprouts operated 440 locations in the latest quarter. It has opened new stores at a rapid clip over the last two years, averaging 5.7% annual growth, much faster than the broader consumer retail sector. This gives it a chance to become a large, scaled business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

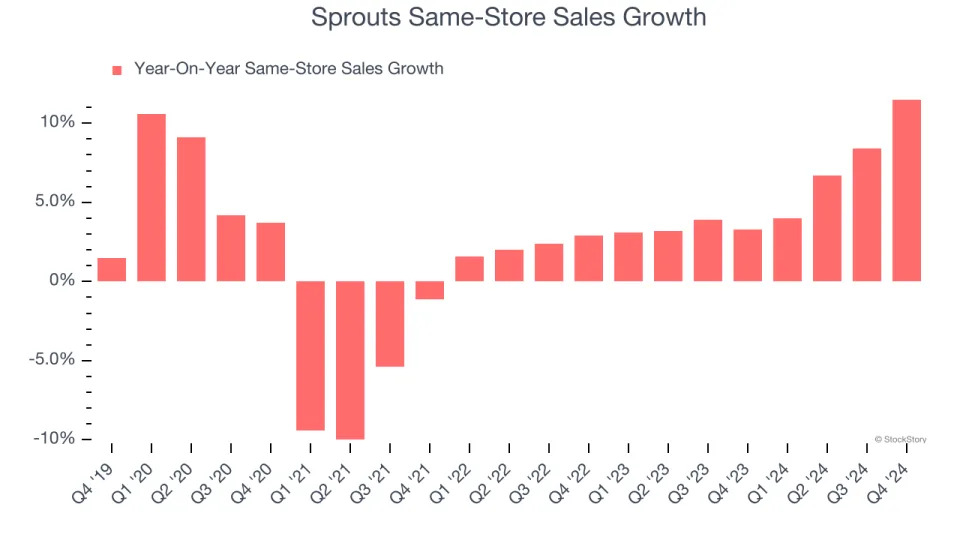

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Sprouts has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing locations. On average, the company has posted exceptional year-on-year same-store sales growth of 5.5%. This performance suggests its rollout of new stores is beneficial for shareholders. We like this backdrop because it gives Sprouts multiple ways to win: revenue growth can come from new stores, e-commerce, or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, Sprouts’s same-store sales rose 11.5% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

Key Takeaways from Sprouts’s Q4 Results

We were impressed by Sprouts’s optimistic EPS guidance for next quarter, which exceeded analysts’ expectations. We were also glad its full-year EPS guidance trumped Wall Street’s estimates. Zooming out, we think this was a good quarter with some key areas of upside. The market didn't seem impressed and perhaps had higher expectations, and the stock traded down 3.2% to $164.50 immediately after reporting.

So should you invest in Sprouts right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free .