(Bloomberg) -- Investors have little room to take advantage of the rally in US Treasuries now, with the Federal Reserve unlikely to cut rates as aggressively as the market expects, according to Mount Lucas Management LP.

Last week the $1.7 billion Pennsylvania-based hedge fund took profit in its discretionary macro fund on a long US Treasury position, which included bonds with maturities between two and five years built up over the last couple of months.

“There’s no more juice left to squeeze from that long bond trade for us,” said David Aspell, co-chief investment officer and partner.

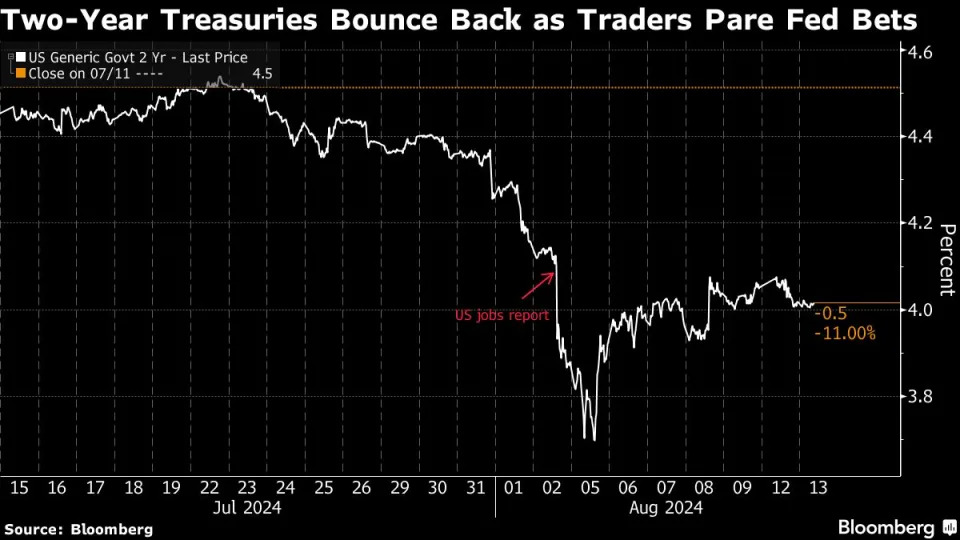

Treasuries were little changed on Tuesday, with the policy sensitive two-year yield trading just above 4%. Traders await a key report on US producer prices that is expected to show the headline annual rate decelerating to 2.3% in July. Consumer prices are due on Wednesday.

Founded in 1986, Mount Lucas runs a mix of discretionary and trend-following strategies. The firm is fully owned by employees, with Goldman Sachs Group Inc. selling its minority stake in 2016. Aspell joined in 2011 from Man Group Plc, where he was a senior risk manager.

The firm’s macro fund is up 5.5% from the start of the quarter through Aug. 9, compared with a 3.7% gain offered by a Bloomberg gauge of US Treasury returns.

Treasuries rallied earlier this month, fueled by a weak July US jobs report. That led money-market traders to wager on as much as 200 basis points of easing by May next year, before paring bets to around 170 basis points.

Still, Aspell is skeptical that the Fed will ease policy on this scale and took an opportunity to sell Treasuries as a result.

“We’re moving to a point where it will be quite hard to outdo the market,” he said.